Saturday, December 24, 2005

Merry Christmas

A friend and client forwarded this email to me. It details many elements of the Christmas season and their meanings throughout history.

Merry Christmas to all, and to all goodnight,

http://www.deerlakemail.com/teach/

Monday, December 12, 2005

Valuation, Valuation, Valuation

I get people fussing with me all the time about the merits of dividend investing. These conversations go something like this: "The bottom line to me is the bottom line on my account statement," they say. "Dividends might be real money and be predictable, but they are not what makes a good investment. A good investment is one I buy low and sell high. Price growth and only price growth matters to me." If I hear this once a month, I hear it a dozen times a month. I hear it so often that it makes me think, I might have the privilege of working in this business for a long time because this kind of thinking is shortsighted, ill-informed, and costly.

Here's my bottom line. If you don't know what makes a stock go up, what good is the price rise to you. When do you take the profit--too soon, too late, never? The markets being what they are, the price will in time go down, and you won't understand that either. So you will cycle between "feeling" good when the market goes up and "feeling" bad when it goes down and have absolutely no idea which of your feelings is accurate. Moreover, as it relates to feelings and the stock markets, most likely neither of them is correct. Feelings are not facts in investing; not yours, not mine.

To escape the cycle of feelings and get connected to reality, you must develop some understanding of how to value a company. I have spent 20 years trying to do this, and my research shows that for many large companies the level and growth rate of their dividends is the best indicator of value. If you study the relationships between dividends and stock prices, you will be surprised by two things: 1. dividend trends are very consistent and persistent and much less volatile than prices or earnings; 2. and yet it is clear that prices follow dividends and not the other way around.

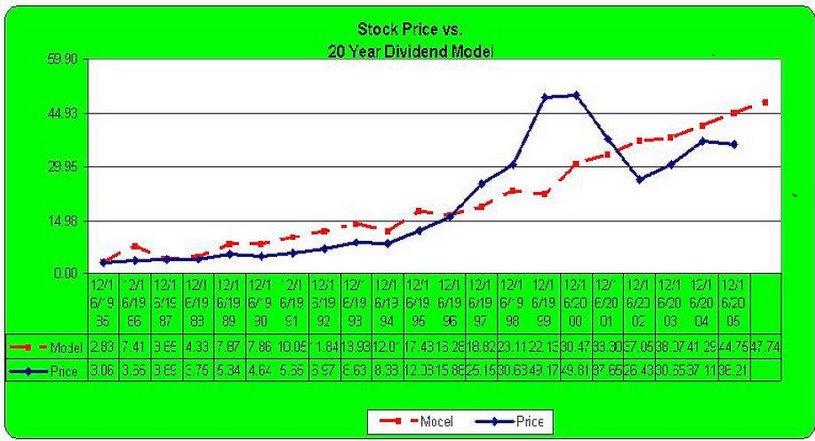

The Dividend Valuation chart below of General Electric is a good example of what I am talking about. The red line is our dividend valuation model for GE over the last 20 years. The Blue line is GE's actual price over this time. Many things are obvious with even a casual glance at the chart: first, the valuation line (red) is virtually a straight line, while the blue line showing price has been all over the road; second, the volatility of price has carried it back and forth across the valuation line; third, buying GE when its price was lower than its valuation line and selling it when its price was above the valuation line has been a near fool proof long-term strategy for the stock. Our rate of return is even better if we buy when price is 10% below valuation and sell when price is 10% above valuation. Finally, the chart shows that the model is signaling that GE is currently selling far below its valuation line, which would suggest it is a good buy. In fact the model is showing that GE is selling nearly 25% below its valuation line. Understanding the model as I do, the only way that the price of GE will now close the 25% gap is if its dividend growth slows dramatically or interest rates sky rocket, neither of which I believe is a strong possibility.

Investing always involves risk, but determining the value of a company keeps you from making emotional decisions that have little chance of success. But of even more importance is understanding value keeps you from getting shaken out of a cheap stock just because the price is going against you.

Someone is always trying to tell me I should be buying this stock or that one. When I ask why, the answer is almost always the same: "Because it's going up." Looking at the chart below, there were a lot of people who were touting GE in 1999, who are still underwater. But there is good news. By my calcuation, they will be back to break even in 2007.

-------GE Dividend Valuation Chart-------

Friday, December 02, 2005

UTX -- Of Horses and Hoods

I'm going to provide a look under the hood of one of our stock valuation models using United Technologies (UTX) as an example. Since 1988 the combination of UTX's dividend growth and the change in interest rates on a 10 Year US T-bond have explained 92% of the annual price movement of the stock. That model currently estimates that the current fair price range should be between $60 and $70 per share, with $65 being the midpoint of the range. UTX is now selling for $55 per share.

At today's price that puts UTX at as great a discount from expected value as at anytime in the last decade. But does that mean it is a table-pounding buy? Yes and no. The expected price range is well above UTX's current selling price, but a look at UTX's history shows that it has had periods of under and over valuation lasting up to 3 years. I fully expect UTX will reach $65 per share over the next few years, thus the question in my mind is not if, but when.

If UTX reaches $65 in the next year, it will produce a total return of approximately 18%; if it takes two years, we will make a little less than 9%. The reason I believe the odds favor UTX reaching $65 sooner rather than later is because UTX has already been undervalued for the past 12 months, so the averages are in our favor.

I just spoke to the company last week and tried to pry out of them what their dividend hike in 2006 might look like. They were noncommittal, except to say a dividend hike was likely in the first quarter. I told them they had enough free cash flow to choke a horse, and I thought their shareholders would applaud, another big dividend hike and a public statement about future hikes.

The company representative with whom I spoke was so used to talking with Wall Street analysts, who completely ignore dividends, that he seems a bit startled when I told him I would rather have the dividend hike than share buy backs.

I mentioned that I had read where the company was disappointed that its stellar 2005 results had largely been ignored by the market, I suggested that a commitment to a dividend payout ratio of 35% would do wonders for the stock price. He was a very pleasant man and said he would pass on my suggestion.

Let's put this one on our radar and see what the next dividend hike looks like. UTX is in our Rising Income Portfolio. Illinois Tool Works, which has a very similar story, is in our Blue Chip Growth Portfolio. I'll review it next.

Wednesday, November 30, 2005

The Evansville Client Dinner -- It was a Blast

Donaldson Capital held its annual client appreciation dinner in Evansville last night. The event was held at the Evansville Museum of Arts and Science. We ate a wonderful meal surrounded by beautiful art and artifacts. Everything went great except for our Texas friends hanging their coats on a piece of contemporary art, which they mistook for a coat rack.

Mike Hull offered our thank yous to clients old and new and shared a bit of our strategy for the future. I cut my speech in half at the request of some of the oldtimers, who said the wine, hors d'ouevres, and conversation were more fun than speech making. I have to agree, but I still got my 8 charts on the wall which showed some of the research that we have conducted on dividends and their correlations to prices.

It was a great night, and the only person I saw nod off was JWB (he's heard it all before). For those of you who were there, that is the reason I had to pick on him a little. He's promised to get his beauty rest next year.

Blessings to all of you. You are our only reason to be. You humble us with your kindness and your trust. We are deeply honored to serve you.

As I said earlier, we will be having other dinners in cities where we work in the months ahead.

Monday, November 28, 2005

Christmas Will Come

The Dow Jones has rallied almost 800 points since mid-October to stand at near 10,900 and many of our clients have asked why? Not that they don't appreciate the bounce, but they question if the news has really improved as much as the rise in prices now reflects.

First, let me remind you that our most reliable model has been pegging the value of the Dow at near 11,800 for most of the year, so a part of this bounce is based on stocks having gotten very cheap, especially when you consider that earnings and dividends have grown at double digit rates. I don't believe that stocks will rise to 11,800 is a straight line, but I do believe there is a high probability that the path of stocks will intersect that level within the next year.

The main reason stocks are doing better, though, is as a result of the economic data that have been released since the conclusion of the Gulf Coast storms. It resolves many of the questions that we cited in our October quarterly letter that need to be answered. 1. The US economy, contrary to the doom and gloomers, has not been materially affected by the storms , and certainly is not headed for recession. 2. Oil prices have softened dramatically to $57 p/bl, down from over $70 p/bl. 3. Inflation spiked in September, but was flat in October. With oil at the current level, November's reading is likely to be tame, as well.

The market is now rubbing the worry beads over the Christmas selling season. I'm not as concerned about Christmas sales as most. My friends in the retail business have told me for years, that everyone always worries about the Christmas season because it is such a big deal to total retail sales in such a short period of time. But they say not to worry, Christmas always comes. It is a part of our culture.

Terrorists, hurricanes, tornados, war, oil shocks, political battles -- all these forces show us just how precious and fragile our lives really are. Christmas and Hanukkah remind us that there is Someone bigger and wiser than us, Someone who has blessed us down through the ages in spite of our folly and the vicissitudes of nature.

Giving gifts to someone we love is as natural as breathing. Do we stop breathing because of the forces we face? Certainly not. Indeed, we will give more purposefully, perhaps more generously, because we will see the faces of those we love, and we love to see them shine. And shining faces have been in short supply during the past many months.

I also encourage you to give to faces you do not know or love. These faces may have borne the brunt of the storms or man's inhumanities to man. A gift from a stranger is almost too good to be true. You will likely never see the face of a stranger light up when they unwrap your gifts, but you know as well as I do that the shine will come -- it's a part of every culture, a part of being human. And you will become a blessing and blessed in the same moment. How can you beat that deal?

Wednesday, November 23, 2005

Thank You

The pastor of my church ends each service with a beautiful blessing:

"May the Lord bless you and keep you; may He make His face shine upon you, and be gracious to you; May the Lord lift up his countenance upon you and give you His peace. Numbers 6: 24-26.

At this Thanksgiving season, I want to express to you how grateful all of us at Donaldson Capital Management are that you have chosen us to work for you. You are a blessing to us. We are honored by the trust that you have extended to us, and in everything we do, we seek to be worthy of it.

Happy Thanksgiving,

Greg Donaldson

Sunday, November 20, 2005

Dividends Talk -- GE -- What More Can They Say?

GE announced a 14% dividend hike last week. As usual the news of this hike was like a piece of juicy gossip. It traveled all around the world before Chairman, Jeffrey Immelt, could get the whole sentence out of his mouth. **Not**

No, the truth is the news of the dividend hike did not even make some financial websites that I watch. And yet, in the few words it took to announce the hike, GE said more about the coming year than a stack of Wall Street research reports. Before I discuss the implications of GE's dividend action, let me show the blog I wrote on December 13th of 2004.

December 13, 2004

So goes GE . . . .

GE's announcement of a 10% hike in its dividend this week is very good news. GE has long been a bellwether of the US economy, and the double digit increase is a plus not only for GE, but also for the entire US economy and stock markets. CEO Jeffrey Immelt also announced future earnings growth in the range of 10-15%%. We believe this guidance says three things: 1. Earnings will grow faster than 10%, 2. Dividends should also grow at least at 10%, and 3. Average US profit growth should be also close to 10% over the next few years. More importantly, GE's dividend and earnings growth pronouncements allow us to compute its intrinsic value. Starting with a dividend of 86 cents,growing at 10% per annum over the next five years then gradually slowing it to a long-term growth rate of 6.0%, all discounted at 9%, produces an intrinsic value of just under $42.00. We think its just a matter of time before the stock trades there. It is currently trading at $37.26. This is the best news on dividends I have seen in a long time. GE is so big and so important to our economy that their guidance sheds a light on the whole economy. Well done Mr. Immelt.

GE had been wallowing around ever since Jack Welsh left the throne, and the 10% hike, to me, was a clear indication that Mr. Immelt was signaling that things were about to get better.

With regards to the three things I said the dividend hike was implying, (1) GE's earnings, indeed, will be above 10% for 2005, at near 13%;(2) The 10% 2005 dividend hike is now being followed by a 14% increase for 2006 (I continue to think 10% will be a floor for the next several years); and (3) US corporate earnings growth will be near 14% for 2005, well above my projection of 10%, which was 50% higher than Wall Street consensus estimates.

The only part of the December 2004 blog that has not come to fruition yet, is GE's price. I said in the December blog that our dividend model was producing a present value of $42.00 for GE. Well, not only is GE not trading at $42 per share, it is actually trading at $36 per share, lower than it was last December 2004.

If you are a momentum investor, you don't care a twit about talking dividends, or valuation. You care only about price, and "what have you done for me lately." But if you are a dividend-value investor, you know that prices and values can disconnect for long periods of time, but sooner or later GE is going to not only trade at $42 per share, but it will also trade at $47.00, which is what our dividend model says it is now worth.

In my judgment, GE is the most important company in the United States. They are very large and so diversified that they are a bit of a microcosm of our entire economy. If GE is upping its dividend and earnings targets for the coming year and thereafter, I believe it is unwise to be too pessimistic about future economic and profit growth for the whole country .

The terrorists cannot stop our economy, the hurricanes cannot stop our economy, even the blood sport that the politicians are playing cannot stop our economy. A year ago the best clue we could have used to tell us the shape of things to come was GE's dividend hike. I think you can do the same today. The only difference is I strongly believe GE's price will catch up with its valuation over the next 12 months.

Friday, November 18, 2005

Odd Lots

Template Change

Ok, so you noticed that the template for the blog has changed. That was not an aesthetic decision that was gremlins on Google which dismembered the custom template I was using and left it unusable. Since I am not much of a techie, I, along with all the king's horses and men, could not bring the template back together again. The template I am using now is a standard version that is idiot proof. I have a cry for help into Google, but with 40 million people using the service, it might . . . be forever before I hear from them. In the meantime, I'll be orange for a while. The red template was just to hot for a conservative money manager.

Client Appreciation Dinner -- Indianapolis

The DCM team just returned from our client appreciation dinner in Indianapolis. It was just wonderful to see old friends and new. We had a full house and everyone was particularly interested in our presentation for the evening which was entitled: Retirement Roulette. We will be having our Evansville dinner at the end of this month. If you are a client from outside the Evansville area and would like to attend, please call Carol Stumpf at 800-321-7442. We are planning client dinners in Birmingham, Alabama and other cities where we work right after the first of the year. I am pretty sure we will continue to speak about the looming problems facing retirement. I will put the highlights of the speech I gave in Indianapolis on this blogsite in the coming weeks.

Market Comment

All the major indices are approaching 2005 yearly highs. The market is doing what it always does -- climbing a wall of worry. In this case, I believe it is way over due. As I discussed in a previous blog, only by using the actual inflation rate could you justify a Dow Jones of near 10,000. As PPI and CPI came out this week and showed inflation had dramatically receded, stocks have pushed much higher and are now positive for the year.

I said in Indianapolis that I believe the Dow is at least 1,000 points undervalued. It will take more good news on inflation to get there, but I have little doubt that we will see a Dow Jones of near 12,000 in the next twelve months, unless something catastrophic happens.

Thursday, November 17, 2005

Dividends Talk -- Northern Trust

Northern Trust hiked its dividend 9.5% today. That was about in line with estimates, though a bit lower that our model was predicting. Northern Trust derives 75% of its earnings from fees, most of which come from wealth management. They have a unique franchise and brand in the money management business: they do business with the super wealthy. They have it down to a science because all banks know what they are doing and, yet, no other bank has been able to duplicate Northern's success. Lots of rumors are constantly circulating about a bigger bank buying NTRS, but there are at least three reasons why NTRS will likely remain independent. 1. They are growing rapidly and few other banks could offer them stock that would have the growth potential as does NTRS's stock; 2. They are not cheap; and 3. They don't want to sell out.

No matter, we think they are just fine on their own. In our judgment they have the most focused, most understandable strategy of any bank in the US. When, as, and if the stock market regains its uptrend, NTRS is a huge benefactor. They have solid organic growth, and a rise in stock prices would give them an added boost. NTRS is in our Blue Chip Growth Portfolio.

We rate Nothern Trust's dividend hike, neutral.

Thursday, November 10, 2005

Stock Market Models--Which One to Believe?

I have been mystified all year that large cap stocks have not fared well. I know there have been headwinds: oil prices, terrorism, natural disasters, political intrigue, inflation, and interest rate hikes by the Fed. But, my work has indicated that the surprisingly good economic and earnings growth should have been able to overcome the headwinds. Corporate Earnings for the S&P 500 are likely to be near 14% above last year, almost twice what many analysts were forecasting at the beginning of the year. Dividends will likely rise 12%, well above projections; and GDP is likely to grow near 3.7%, again, well above the estimates at the beginning of the year. I cannot remember the last time such good economic and earnings news was so totally ignored.

My most reliable valuation model, which looks at the historical relationships between price, dividends, and interest rates, currently points to a fair value for the Dow Jones of 11,800, over a thousand points higher than the Dow's current level. This model has been able to explain nearly 95% of the annual movements of the Dow over the last 45 years. A second tool, our dividend discount model, which computes the present value of future earnings and dividend growth, says the intrinsic value of the DJ30 is over 12,000. Both of these models are time tested and have seldom been wrong for lengthy periods of time. But they have been overly optimistic in 2005.

In attempting to understand why large cap stocks have utterly ignored their excellent fundamentals, I fell back on one of my old models, the P/E model. I stumbled across this simple relationship between P/E and inflation in the early 1990s. It has not been as precise as the other two models, thus, I don't spend a lot of time with it. This model does not pay much attention to projected earnings, dividends, or interest rates. I have tested them in the model but they do not improve the model's correlation with actual price to earnings ratios.

The formula uses only the Consumer Price Index and a 3% premium. Here's how it works. To find the appropriate P/E for today's market you add 3% to the current rate of inflation. The current CPI core rate of inflation is 2.3%, year over year.

3% +2.3% = 5.3%

This produces an expected 5.3% earnings yield (E/P) for the today's market. To determine the predicted P/E ratio, we divide the expected earnings yield into 1.

1/5.3% = 18.7X P/E (Projected)

The formula says the Dow Jones should be trading at 18.7 times trailing 12-month earnings. With last the last 12 months DJ earnings at $650, that produces a price of 12,155 for the Dow. That's great, but it does not help us understand why stocks are selling at only about 16X earnings.

Then it hit me. I did all the original research on the P/E model using the actual average annual CPI, not the core CPI. The core CPI, which excludes food and energy, is the measure of inflation that is most used on Wall Street because it is less volatile;it is also the inflation indicator that the Federal Reserve watches most closely. As I was thinking about this, it occurred to me that the relentless rise in oil prices may well have tipped the scale in favor of investors using the actual CPI instead of the core CPI, because they may have come to believe that oil prices and inflation are only going higher. They may have also abandoned using the core CPI because the difference between it and the actual CPI is as wide as it has been in decades.

Over the last 12 months, the actual CPI has averaged 3.4%. If we insert this figure into the data, we get the following result.

3%+3.4% = 6.4%

1/6.4% = 15.6X P/E (Projected)

15.6 X 650 = 10,140

Yikes, that is not very encouraging, yet the DJ 30 did touch 10,156 in mid-October just after the hurricane-induced spike in inflation. It was also at about that time that investors became more worried about the economy and earnings because of the possibility of rising interest rates. Thus, the terrible storm along the Gulf Coast have created a kind of perfect storm in the financial markets. The Katrina, et al, spiked oil prices and inflation and which dampened prospects for economic growth and profits. Even though I wrote here and elsewhere that oil supplies were fine and that the economy would weather the storm without great effect, apparently the stock market was not buying my argument(it seldom does in the short run). But, in recent weeks as economic and corporate growth data has shown only a modest impact from the storm, the market has shaken off much of its lethargy and begun to rise.

So what do we believe, the simple, old fashion P/E model that uses actual CPI and says stocks should be having a tough year, or the P/E model that uses core CPI and says stocks should be 12%-20% higher?

The world thinks the value of a stock is what it is selling for today. I do not believe that, and I can show you proof after proof that, during times of crisis, the stock market almost always goes the wrong direction at first, before recovering it senses and more accurately pricing earnings and dividend growth.

With oil prices now at $57.50, well off peak their peak of $70+ per barrel, the CPI should moderate dramatically in the coming months. I predict that by the middle of 2006, the CPI will be below 3% on a average year over year basis. The reason is simple, the Fed's target for inflation is about 2%, and moderating oil prices will help them get there.

For your information, I have provided below a chart showing the actual P/E vs. the level projected by my simple PE Model. I think you will agree that the model has done a surprisingly good job of capturing the trend of the actual PE. It will change again next week when new CPI data come out. I'll report here what it looks like then.

Thursday, November 03, 2005

Dividends Talk -- Emerson Electric

I am on the lookout for the dividend increases of important dividend-paying companies. My belief is that in these post-hurricane times, the amount of the increase will say as much about the future as the past. Thus far, I have commented on Paychex, a payroll processing company, and Carnival Cruise Line, an entertainment company. Both blew away their dividend estimates, which is important because both companies offer a glimpse of the thinking of corporate America about the prospects for the coming year.

Emerson Electric -- EMR raised their dividend 7.2%, or about three times what Value-Line was estimating. EMR is a major industrial company providing process management and industrial automation to companies worldwide. It is a clear Dividend Star, having increased its dividend for over 48 years in a row. Earnings grew 18% for the quarter, which was also above the estimates.

The reason EMR's above-estimates dividend hike is important is because they are are a leading company in the capital goods sector, which has been very strong in 2005. Some people are worried that this sector will slow in the coming year due to a slowing worldwide economy, resulting from rate hikes in the US and abroad. While I believe EMR could have increased their dividend just a bit more, they do have a stated dividend policy and the 7.2% increase was within those guideline.

I'm going to rate the EMR dividend increase as neutral. We'll keep a running score on dividends hikes for a few months. So far

Dividend Scoreboard

Number of positive surprises 2

Number of neutral increases 1

Number of negative surprises 0

Sunday, October 30, 2005

Economy Watch -- What's Right with This Picture?

There was big news on Friday. News that was a shock to us all. News that changes paradigms, mind sets, and bottom lines. News that assaults our notion of "what's going on 'round here." This news had nothing to do with Scooter Libby or the bloodsport that politics has become. This news was so good, that I could find almost no mention of it in the Sunday version of the New York Times, and it generated only a brief mention in my local paper. This "good news" that the media chose to ignore was that in spite of the hurricanes, the US economy grew at an inflation-adjusted rate of 3.8% for the third quarter. Remarkably, this was a higher rate of growth than the previous quarter's 3.3%.

Pardon me, but I thought Katrina et al, were sending us into certain recession. Isn't that what the "Main Stream Media" told us; isn't that what the headlines in your local paper said?

There is something else the MSM is not reporting: strong corporate profit growth of nearly 13% vs. a year ago. The odd thing about this is one of the few industries that is in a recession is the media business. Newspaper circulation is plummeting, network television viewership is collapsing, and movie theatre box office receipts are trending lower. Maybe that is the reason the media in this country are so disconnected from reality in their reporting, they are depressed from observing their own fate. This is the opposite of the orchestra playing waltzes as the Titanic sank. The MSM are like the choir singing dirges on Easter morning.

Stay tuned, I'll keep you informed about the true state of the economy and profits. There are lots of economic releases coming. We expect some softening, but, as we said in our recent quarterly letter, the downtick will be followed by a big uptick as the rebuilding of the damaged areas reaches full speed.

Thursday, October 27, 2005

Dividend Talk - Carnival Cruise Lines

I have been watching recent dividend increases from large corporations for clues they might offer about the company's projections for the year to come. In some respects, we are flying blind with regards to the real strength of the economy and corporate profits because of the disruptions of recent storms.

I took a very positive read from Paychex's 23% hike a few weeks ago, because of its implications for employment. Today I take another positive read from Carnival Cruise Lines. This week CCL hiked its dividend 25%. Our dividend discount model was estimating a 13% hike and Value-Line was estimating a 7% increase.

Let me see here, let me count the ways that CCL is in the eye of the storm. 1. Many of their main bases of operation are along the coast of the United States; 2. They consume huge quantities of petroleum; 3. They do not sell an essential service, and their customers have to travel long distances to reach them; and 4. They have a terrorist threat because cruise ships are a known target.

This does not sound like a recipe for surprisingly good news, but their 25% hike is just that. Again in my judgment, as in the case of Paychex, a 12%-13% hike would have been fine with investors and Wall Street. So, why a 25% dividend hike, unless it says something about next year's business? They know they are in the eye of the storm. They know the aforementioned four points. They go to bed with them every night and wake up with them every morning. I believe the answer to that question is obvious: Come heck or high water they think their business is going to be better in spite of the obstacles than does Wall Street, and in my judgment they are putting their money out to prove it.

This kind of dividend talk is priceless, because it is tangible, comes from the source, and, finally, because most people ignore it.

We do not own CCL in any of our styles of management, but as a result of this dividend action, we are studying it very closely. We'll comment later on our final decision, but either way, as a signal, CCL's hike is valuable.

Monday, October 24, 2005

I'm for Ben

Today Ben Bernanke was announced as the successor to Federal Reserve Chairman Alan Greenspan and the Dow Jones jumped 170 points. Wall Street is voting with their dollars and it is clear they like the new man. This morning before the announcement, I was asked by a friend about the strong rumors that Bernanke was going to get the job. I said that ever since he was appointed Chairman of the Council of Economic Advisors, he was considered the front-runner for the job, but I was surprised that he was apparently getting it, and I thought it might take awhile to get used to him. He was a virtual unknown among investment people even 4 years ago. He had built a strong reputation in academic circles while at Princeton University for his study of the Great Depression and the Fed's role in it.

My friend said what is your gut feel of the guy? I said three things come to mind immediately. He is said to be utterly brilliant, he is a strong believer in encouraging the private sector to grow the economy instead of the government, and he is a bit of an unusual duck.

I'm guessing the stock market's uptick today was its approval that his positions are considered to be along the lines of Alan Greenspan's. He is considered by many as a supply side proponent, meaning he favors low taxes on income and capital gains.

His brilliance was on display when he began talking about the possibility of deflation in 2002 and 2003. It is dangerous stuff to talk about deflation because the word in many economists' minds has a direct link to the depression. When he was not shouted down by the economic elite of this country, it was clear that, even though I did not know who he was, the power-elite did. I remember I had the clear impression that his statements were so bold that he would not be saying them if they did not have the blessing of Alan Greenspan. When I looked into who Ben Bernanke was, I found a somewhat unusual man for the job of operating in the public light. He wore a beard and did not like to wear suits. He wore cowboy boots and rode a motorcycle. I remember the Wall Street Journal commenting that if he were to become Fed Chairman things would be a whole lot different during Fed reports on capitol hill. Whereas Mr. Greenspan would humor every question and drone on for indeterminable minutes on the esoterics of economics, Ben did not suffer fools well, and his speaking style was short and . . . short.

Today's Wall Street Journal had a funny piece about President Bush noticing that Ben had on light socks with his dark suit at a formal occasion and suggesting to him that black socks might be more appropriate. At the next Council of Economic Advisors Ben arrived early and passed out light socks to all the members, who were then wearing them when the president arrived.

Ben Bernanke is a character, but he is no fool, and he possesses one of the great minds of our time on economic theory and how to apply it in the real world.

I have been a fan of Alan Greenspan's since the beginning. I remember that rumors appeared soon after he was appointed Fed Chairman that outgoing chairman Paul Volker did not think he was tough enough to handle the politics of the job. I'm glad Mr. Volker was wrong. The same questions will, no doubt, be asked of Ben Bernanke. Time will tell, but most guys I know who ride motorcycles are not all that easy to push around.

If white socks can give the market a boost, count me in, Ben.

Monday, October 17, 2005

Thank You Brian Wesbury

Brian Wesbury is the Chief Economist at Claymore Securities in Chicago. He is a frequent contributor to the Wall Street Journal and other publications. I think you could describe him as a supply side economist. I have followed him for years and find that he offers a very fresh voice in a world too full of the weary dronings of the prophets of gloom and doom. His most recent weekly investment letter is so right on that I am sharing it in its entirety.

Risk-Phobia and Faith

Throughout history, adventure and risk-taking have led to great progress and wealth. Early explorers risked their lives sailing rickety ships, negotiating mountain passes and experimenting with new medical procedures. Of all countries, the United States has most embraced this model of progress.

The results have been nothing short of miraculous. In the past 200 years, the number of people living in freedom, and not tyranny, has grown exponentially. US life expectancy has doubled over the past 100 years, while others have seen life expectancy grow more. While relative poverty is still with us, in most industrialized nations the lowest incomes still afford a lifestyle better than royalty had in the past.

Technology allows us to see storms before they make landfall. Helicopters rescue terrified citizens from rooftops afterward. Computer-based risk management systems allow companies to find workers after a calamity, re-open businesses faster than ever before and move essential supplies to people who need them.

While we will never conquer calamity, all of this saves lives and reduces risk. Despite four major hurricanes in 2004 and two monsters in 2005, the US economy continues to grow as it absorbs the damage.

On the other hand, attempts to use government to reduce risk have not succeeded. The levees in New Orleans did not work as they should and intelligence systems failed at detecting the plots of 9/11. At the same time, Sarbanes-Oxley did not stop the CEO of Refco from doing immense damage to the firm he was supposed to shepherd.

This does not mean we should not work at improving government. But nothing will quell the sinful nature of man or stop the immense forces of nature. These things, we will always have to live with.

This brings us to the seemingly limitless fear of recent months. Volatility indices have climbed sharply, equity prices have fallen, new tropical weather systems boost oil prices, and fears of bird flu generate hundreds of thousands of words of warning in national news sources. We have no way of knowing whether or not these fears will come to fruition, we do know that history is a story of overcoming such events. We also know that these fears are most often overstated.

Despite these facts, many people continue to look toward government for some reassurance that it can stop bad things from happening. They are succumbing to riskphobia and lack faith that a flexible and free market economy is an efficient shock-absorber. Looking back at the past few years should give pause to excess fear.

The US economy remains robust. Jobs, incomes and profits continue to climb. Keeping faith, while others doubt, leads to progress and wealth.

Brian Wesbury

Friday, October 14, 2005

Economy Watch: The One-Handed Economist

Someone once said that what the world really needs is a one-handed economist. The reason for this pithy statement is because economists are famous for making grand prognostication and then saying, on the other hand such and such could happen, which would give us a completely different outcome. Tomorrow's headlines in your local newspaper will make the case that economists keep their two-handed approach.

The headline will read, "Inflation at 25 Year High." It will be true, but "on the other hand" it will not be meaningful. The 1.2% jump in the consumer price index was almost entirely caused by the surge in energy prices during and after the two storms. The core CPI rate, which excludes food and energy and is the measure of inflation that the Federal Reserve believes is most important, rose only .1%. So take your pick; either we have annual inflation of 14.4% (the 1.2% is a monthly figure) or 1.2%. My belief is that inflation is much closer to 1.2% than it is the former.

I can assure you that the main stream media will get this so wrong that I will be countering their ignorance of this issue for many months to come. So now in addition to monitoring dividends hikes and economic growth, I will be commenting on the real rate of inflation on a regular basis for a while.

This blog is supposed to be about dividends, but we will have to do battle with the forces of dis-information and confusion before the quiet voice of dividends can be heard at all.

At .1% the core rate was actually less than the estimates. The core rate of inflation is so important because it shows the rate of inflation in the 85% of the economy apart from the very volatile food and energy sectors, and, thus, measures the spill over of high energy prices into the rest of the economy. The "one-handed" answer to how much spill over there has been is -- not much. Over the past year, the core CPI has grown by under 2%, while the CPI including food and energy, has grown at near 4%.

If I am correct in my belief that oil prices will cool down as a result of sticker shock at the gasoline pumps, then the Consumer Price Index should begin trending lower in 2006. I realize this flies in the face of the headlines in your favorite news source, but to me it is almost baked in the cake.

Thursday, October 13, 2005

A Dividend Star Does Some Talking

As I mentioned in the last edition, I am very interested in the dividend hikes of major companies during the fourth quarter. This is a time when many companies make dividend increases based, in part, on what kind of a year they have had, but also, influenced by their expectations for the year ahead. Paychex is a processor of payroll checks and human resources outsourcing for small and medium-sized companies. The company is a solid Dividend Star having raised its dividend for 16 years in a row and has the 4th highest dividend growth among companies that have raised their dividends for at least 10 years in a row.

PAYX's dividend growth had slowed to the low double digits over the past 5 years, reflecting the after effects that 9/11 had on employment. However, their business has bounced back, solidly, over the past year in line with US employment growth.

Here's the good news. PAYX just announced a 23% dividend hike. That was twice what Value-line was projecting, and 50% more than our own expectations. In our judgment, this larger-than-expected dividend hike is about as important an announcement as we could hope for in this environment. First, as it relates to PAYX, the dividend hike is at a higher rate than their earnings growth for the year and at a much higher growth rate than their hikes of recent years. The only conclusion that makes any sense to me is that they believe their business will continue to improve. Second, and even more importantly, since they are the second largest processor of payroll checks, and the largest processor for small to mid-sized companies, I believe there is a not-too-subtle message that they are bullish on employment in the coming year.

This is exactly the kind of "signaling" that I believe companies do all the time with their dividends. In this case, the signal carries over to the the economy as a whole, which is vitally important because of the unknowns created by the hurricanes and the oil spikes. PAYX, it seems to me, is giving us a clear signal that they believe (as we do) that the economy will shake off the ill effects of the storms and grow at about the same rate in 2006 as it has in 2005.

As I described earlier in the year, the signaling qualities of companies is a key in our overall analysis of the attractiveness of a company's prospects. Our dividend discount model values PAYX at about $40 per share. With the stock selling at just over $36 per share, it is a reasonable value. It's dividend is not high enough to qualify for our pure dividend style of management, but we do own it in our high growth portfolio.

I'll report again when another major company speaks with their money.

Saturday, October 01, 2005

Dividend Increases Talk

The fourth quarter is one of the heaviest times of the year for dividend increases. Many corporate boards will be announcing to shareholders what part of 2005 corporate profits they will be paying out in dividends. But it is important to remember that dividends are as much about the future as the past. No company wants to set a dividend rate that they will have to reduce should business turn soft. With Katrina and Rita having cut a whole in near term earnings and blurred prospects for 2006, I will be very curious to see what kind of dividend increases we get, particularly for the Dividend Stars. Dividend Stars, you will recall, are companies that have consistently raised dividends for many years, even when dividends were out of fashion.

Also of interest will be the dividend hikes from the oil stocks. Earnings are way up, but dividend increases have not been anywhere close to earnings growth for Exxon and Chevron. Will they share the wealth, or will they keep buying back stock. Stock buybacks are fine, but did you ever ponder the fact that stock buy backs mostly favor people selling out. Gimme the cash, I'll reinvest it if its good enough.

Finally, I will become concerned about forward earnings if we see a lot of the major dividend payers hike payments by 6%-7%. A hike of this magnitude is the long-term trend and is the same thing as a punt.

Dividends talk, and I want some of the key dividend companies, like GE, United Technologies, MMM, Coke, and Pepsi to be hiking payments in the 10%-15% range. In my mind that would be signaling as much about the coming year as the one just past.

I continue to believe that stocks are very cheap relative to bonds, maybe as much as 20% undervalued. With 2005 earnings now expected to rise 12%-13% versus expected growth of 7% at the beginning of the year, most companies have had a windfall year. Will they reward us with windfall dividend hikes or will they revert back to long-term trend hikes in the 6%-7% range?

I will chronicle important dividend announcements on the site through the end of the year. I will provide a list of the lineup in a future blog.

Tuesday, September 27, 2005

The Barnyard Forecast Revisited

On August 18, prior to the Hurricanes Katrina and Rita, we took a look at the prospects for the stock market in the year ahead via our Barnyard Forecast. The forecast is a big picture analysis of the position of the major components of the economy and how they resolve themselves on-balance. You may want to review the previous post for a more expansive explanation of how we view each component.

Economy: In the Barnyard model, economic growth above 3.5% is considered negative because its means the Federal Reserve will be applying the brakes by raising interest rates. Prior to the hurricanes, GDP had been growing at about 3.6%, which we ranked as neutral for stocks. The hurricanes are now expected to chop near 2% off GDP growth over the remainder of this year. That would seem to imply that the Fed's long string of rate hikes is nearing an end, which would be good for stocks. The only problem with this view is that the rebuilding of the Gulf Coast area will provide a huge stimulus to the economy and probably push economic growth in the early part of 2006 back above the caution level of 3.5%. I still rate the economy neutral for stocks, 1 point.

Inflation: This is the wild card in the deck. The stop and go nature of the economy for the coming year assures volatile readings. I believe the core CPI will average near the caution level of 2.5%. This will be neutral for stocks, 1 point.

Earnings: There will also be a stop and go quality to corporate earnings during the next twelve months. With business currently slowed or stopped in the Gulf Coast region, in the near term, earnings will be lower than expected; but the uptick in the rebuilding process will also lift earnings growth next year above 7%, which is the threshold required to achieve a positive score. Positive 2 points.

Interest Rates: I still rate interest rates neutral. The 10-year T-bond is currently yielding 4.25%. That is about the same as it was at the beginning of the year, as well as a year ago. Interest rates could drift a little higher in the early part of 2006, but I do not see long-term bond yields or mortgage rates being much higher a year from now. Neutral 1 point.

Opportunity: The model scores 5 points (1+1+2+1), which is the same as it did on August 18, before the hurricanes. It may be hard to believe, but the hurricanes have done little to the longer-term outlook for growth of the economy or corporate earnings. Certainly, there will be some rearranging, with a slowing followed by a return to stronger growth, but the net effect is a reading that is about the same as a month ago. I do believe, however, that the Fed will stop raising rates in 2006, and as it becomes clear that they will do so, stocks will likely have a strong advance. Stocks are very cheap now. Earnings are up nearly 13% over a year ago, yet prices are down. This divergence cannot hold, and I believe it will be resolved by stocks moving higher.

Wednesday, September 21, 2005

The Fed Interest Rate Hike

With the recent devastation of Hurricane Katrina and another storm on the way, there were many who believed that the Federal Reserve may interrupt there long string of rate increases, in favor of a wait and see attitude. Thus, the stock market has registered its displeasure with the Fed’s announcement of another .25% hike by selling off nearly 150 points. But we believe the stock market has it wrong because a close reading of the news release that accompanied the rate hike contains some good news about the long-term strength of the US economy.

Before we analyze the Fed’s statement, it is important to remember that the Federal Reserve’s responsibility is to set interest rates consistent with maximizing economic growth and minimizing inflation in the long-term. The operative word here is long-term. The Fed’s accompanying statement stated the following regarding the impact of Hurricane Katrina:

“While these unfortunate developments have increased uncertainty about near-term economic performance, it is the Committee's view that they do not pose a more persistent threat. Rather, monetary policy accommodation, coupled with robust underlying growth in productivity, is providing ongoing support to economic activity.”

We believe their statement is very straight forward and very good news. The Fed is the most sophisticated economic data gathering entity in the world. They have looked at this data and other instances of natural disasters, and they have concluded that in the short-term the hurricane’s damage to the overall economy will be readily contained, and the long-term prospects for the economy are still very good.

The Fed is making its decision to hike rates based on its long-term view of things, not the current news of the day. In our judgment, it is this focus on the long-term that has allowed Alan Greenspan and Company to navigate through countless crises during his 18 year reign as Chairman of the Federal Reserve. There are many politicians and media-types, who are lambasting the Fed’s rate hike as being insensitive to the plight of the suffering. To the contrary, if the Fed believes there are untamed inflationary pressures building, they would be just one more body of governmental body shirking their responsibilities if they took a pass.

The stock market and some politicians may not approve of the hike, but we are actually encouraged with the language of the press release and relieved that the Fed believes, as we do, that Katrina will not take the wind out of the US economy in the long run.

Thursday, September 15, 2005

Katrina Changes Things

The Wall Street Journal reported that US gasoline consumption has fallen by 4.3% since Hurricane Katrina hit the Gulf Coast. The Journal went on to explain that few analysts are ready to project a continuation of this trend, but as I said last time, I am. I think the uncertainty of the oil supply is finally reaching the consciousness of Americans, and I believe they will embark on a mini conservation program that will result in a slowing of per capital energy consumption.

For years we have been warned repeatedly that our mobile lifestyle was being made possible by such "rock solid" bastions of democracy as Indonesia, Russia, Iran, Saudi Arabia, Venezuela, and Nigeria. But since there have been few alternatives and oil has remained available and cheap, we have looked the other way. But, oddly enough, Hurricane Katrina has done what OPEC and terrorism could not do: it has shown us how fragile our supply of oil really is.

One big storm knocked out 50% of the refining capacity of this country. Emergency oil supplies have been released and gasoline prices have fallen from near $3.40 gal. (Indiana) on the day of the storm to $2.90 gal. today, but I do not believe prices are destined to go significantly lower in the coming year. Indeed, gasoline prices now have three tail winds pushing them: A terrorism premium, a storm or natural disaster premium, and an emergency supply premium. The first two premia are obvious, but the third needs some explanation. If you are a major US organization with large energy needs, whether you are a government or commercial enterprise, you must now consider the merits of having an emergency fuel supply as a backup for your needs.

This kind of emergency fuel storage build up occurred during the last energy crisis in the late 1970s in very large numbers, as governments, businesses, and individuals installed storage tanks to buy ahead of the perceived inevitable price increases in oil prices, but also to provide an emergency supply of energy. I believe, at some level, this better-safe-than-sorry type of hoarding will happen again. Indeed, the probability of this kind of hoarding would increase dramatically if gasoline prices were to rise above the recent hurricane-induced price spike of $70.

The same motive forces that will compel institutions to add emergency energy storage capacity will also compel consumers to go on something of a energy diet. But more importantly, it will cause a dramatic increase in demand for for fuel efficient automobiles, appliances, and houses. This conservation and efficiency ramp up will not wait on solid cost-benefit solutions, but will spring first from a sense of buying "insurance," and then, as innovations become abundant, will evolve into a kind of Y2K stampede toward smart cars, houses, and cities. Again, the first step will be conservation, but the next step will be a huge increase in demand for high-mileage cars, especially, hybrid cars and diesels.

With home prices in a persistent uptrend in most areas of the US and low unemployment, the average family in this country feels pretty well off right now, and buying a high-mileage hybrid car or a diesel powered car in response to the heightened awareness of the fragility of our energy supply, will trump the normal cost-benefit analysis.

Americans have been awestruck by the devastation and human toll of Hurricane Katrina. But the subliminal message in every heart-rending picture from the storm's aftermath is that those who were able to take care of themselves fared much better than those who waited on the government. I am not slamming the government here. There are enough people doing that. I am just stating that we are a nation of doers. Most of us are in this country because we or someone among our forbearers decided to move on. We are a freedom loving people, and one of our most prized possessions is our lifestyle. Most of us are not willing to move back into the city and use public transportation. Someday smarter cities with a more people friendly attitude may pull that off, but until that happens, we will move heaven and earth to fight for our way of life.

I believe that the cumulative effects of terrorism, unstable or hostile governments in control of the oil supply, and the shocking events of a natural disaster, will stick in the crawl of most people, and little by little, they will take steps to use less energy. It is not something that you will see start tomorrow morning, or next week, or next month. It may not show up in the economic statistics for a long time, but I am convinced a new attitude about energy consumption is underway. It will change the profitability of a lot of industries. We are already making some changes in your portfolios that we believe will take advantage of the new forces at work. When we are finished, I will discuss some of our views on individual companies in more detail.

Next time, I'll take you through an update of the Barnyard Forecast. Not to fear, the forecast for the economy and stock prices is still good.

Saturday, September 03, 2005

Katrina and the Economy - Oil Prices

There has been an odd dichotomy is the energy markets for the last couple of years. By all accounts, the available supply of crude oil has been consistently in excess of the demand, but the demand for gasoline has been nearly 100% of the supply. At first this seems to be a circular statement that makes no sense. That is until you realize that crude oil and gasoline are not the same commodity. The difference, of course, is that gasoline is refined. In essence, there has not so much been an oil shortage, as a refining shortage. Refineries are big and smelly and not welcomed in many areas of the country. The last refinery to be built in the US was the Garyville, Louisiana facility, which started up 29 years ago in the 1976. It was one of the eight refineries shut down by Hurricane Katrina, but reports say that it and three others will be back in operation by Monday. The huge Chevron refinery, which suffered a lot of damage, is said to be nearer to coming back on line than was originally thought.

The release of oil from the Strategic Petroleum Reserve by the President was crucial in bringing some measure of stability to the oil markets. This is because many of he oil production platforms in the Gulf are adrift or damaged and may be months away from operation. Thus the crude released by the President gives vital feedstock to the refineries, which the experts say have been damaged but are mainly awaiting power to come back online. In addition, the International Energy Association is releasing 2 million barrels of crude oil per day to the US. These two sources of crude oil pushed crude oil prices down by nearly $2 on Friday to approximately $67.50.

I am not as worried about the energy situation in the short run as are many analysts. My reason for modest optimism is something called the elasticity of demand. This is a very basic concept in economics that says as prices rise, demand slows. Many of the commentators that you hear spouting about oil prices going through the roof believe that oil consumption is inelastic. That is, oil consumption is not responsive to price. History would appear to be on their side because oil consumption has, indeed, risen over the years, even in the face of rising prices. Where I differ from these commentators is that it has been my observation that things change during crises. Crises make people stop and think. You might say tough times make people count the costs. With gasoline prices at $3.40 per gallon and the horrors of Katrina fresh in our minds, in my judgment, prices will bite and oil consumption will begin to moderate.

I want to keep reminding you of what happened the last time we had an oil crisis that actually reached the consciousness of the American people. That was in 1979 during the Iranian revolution. The Shah of Iran had fled the country and the radical Islamic Ayatollah Khomeini and his followers seized power. They may have known something about revolution, but they knew nothing about oil production, and Iranian oil production collapsed, causing oil prices to skyrocket world wide. Because American's saw prices explode and realized supplies were likely to be uncertain for a long time, they began a conservation and substitution campaign that was utterly remarkable. In 1979 the US imported 32 million barrels/day of oil from OPEC. Three years later that figure had fallen to 19 million barrels/day.

I don't foresee a pullback in consumption of that level, but I believe Americans will begin to become more conscious of their gasoline consumption and in doing so their consumption will slow. This sounds like a bold statement without much to back it up, but I have observed time and again that when events appear to be spiraling out of control, people will almost always insert their own attempt to control events. There is only one thing they can do: cut back on consumption, and I think that is what they will do.

I still believe the economy will dip between now and the beginning of the year, but I completely disagree with those people who are calling for a recession. In my mind, that would be almost an impossibility. Prior to Katrina, most estimates had GDP growth above 4% for the third and fourth quarters. I do not believe it is possible to shut down an $11 trillion economy so fast as to push us into recession. I expect the economy will be accelerating by the early part of 2006. The rebuilding of the Delta region will be a massive stimulus to the economy for the foreseeable future.

I admit that my view of the unfolding events is optimistic. I think you also know that my attitude is that most people overestimate the negative effects of natural disasters. My experience tells me as bad as things may seem, repairs will be made, the lights will come on, the water will leave New Orleans and a rebuilding process will begin. The only obstacle I can see that would slow the coming economic stimulus is if a debate breaks out about the wisdom of rebuilding a city that lies below sea level. I am hearing some rumblings of this. If it becomes widespread, the rebuilding may be delayed until next spring. If that were to happen, the economy will slow after the first of the year. I'll have more comments in the days ahead.

Monday, August 29, 2005

Katrina and the Economy - I

I have held up publicly commenting on Hurricane Katrina for the last two days because it did not seem right to me to be talking money when so many lives have been lost or dislocated. However, I have spoken to many of you, and I think it is appropriate that I pass on to everyone my thoughts of the short and long-term implications of Katrina. The history of natural disasters has followed a fairly regular course. There is a short-term dip in economic activity followed by a strong uptick 3 months to 12 months later. It may seem impossible that anything good can come out of such a destructive storm, but from a pure economic perspective, once the rebuilding begins there is a significant economic stimulus.

I think the best way to understand this is to think of the economic implications of one family. For our purposes here, let's call them Mr. and Mrs. America. The Americans lived in a 30-year old home on a side street in a pleasant middle-class neighborhood. Their children are gone, and they both work outside the home. The storm's winds have completely wrecked their home, and they are living with friends in another part of town. We will assume that they will continue to receive their salaries from their places of employment.

They have been in contact with their insurance broker and they have been told that they will be receiving a full settlement of $240,000 for their house and $50,000 for contents. They will also be receiving some bridge type support for living expenses while they rebuild. They have already talked with a contractor friend, and he has agreed to rebuild a home with approximately the same square footage and improvement as their old home. Some additional improvement they would like will add another $25,000. The biggest problem they have is that their street is still covered with water, and it will take weeks to clear the damaged trees and houses in their neighborhood. They could begin work much sooner if they rebuilt in a more suburban area farther from the center of the city. Thus even though they have a check waiting for them at their insurance office and a contractor ready to go, they must wait. The only thing they can do to get their lives back to some semblance of normalcy is to begin the process of shopping for the essentials that they know they will need, such as sheets, towels, and everyday clothes. They have leased a storage unit, and they plan to go shopping at a nearby Walmart that is powering its facility with a generator.

To get at the implications of the storm's effect on the economy of the area, we have to make two estimates of the American's annual spending. The first is the amount they spend annually on the contents of their home. and the second is the annual maintenance cost on their home. Because they will still be eating and brushing their teeth at about the same rate as before the storm, the biggest change in their family expenditures is the money they would ordinarily be spending on their total living expenses that is now in suspension.

Let's assume that the $50,000 they received from the insurance company for the contents of their home has an average life of 5 years. That means that the American's spend an average of about $10,000 per year on clothes, furniture, decorating, electronics, and appliances. That is an average of about $800 per month. To keep things simple, let's assume they have no mortgage on their house. The $240,000 they received for their home would have had an average life of 40 years, meaning maintenance and improvement on their home would have been about $6,000 per year, or about $500 per month. Finally, they spend about $700 per month on utilities, telecommunications, cable, and insurance. The items total about $2000 per month. This represents about 50% of the American's take-home pay. With some possible exceptions, the remainder of the American's expenditures will continue as before.

If this 50% hit to spending were wide spread across the area, the economic implications for the New Orleans area would be devastating. Economically speaking, Mr. And Mrs. America would be fine: they have the insurance proceeds to replace their home and belonging, and they still have jobs. But the storm has essentially cut their spending by half for as long as the damage takes to clean up, and thus, the economy in the area will suffer.

The ironic thing about the American's situation, however, is their current shortfall in spending will be more than made up over the next 12-18 months. At some point over the next 18 months, they will be spending the insurance proceeds of $240,000 plus the additional $25,000 for the improvements on their new home. In addition they will be spending the greater part of the $50,000 they received for the contents of their home. Looking at it from another perspective had the storm not occurred, they would have spent about $24,000 on items related to their home. Now, because the storm has destroyed their home, they will be spending $315,000. Multiply this times thousands of people and the Delta region will resemble a boomtown.

In essence, it is hard to believe, but these natural disasters can actually spur economic activity on a delayed basis. For this reason, I do not believe the economic impact of the situation will be anywhere near as bad as some are now warning.

The real risk to Katrina is the damage she did to the oil infrastructure in the area. I will not cite statistics that you can easily find elsewhere, but there is heavy damage to the offshore oil rigs as well as the refineries. I can not speculate on how much damage there is, or how long it will take to repair it, but I do know that the refineries in this country were already running near capacity. Thus, even if one refinery is severely damaged, the supply of oil will be cut and prices will rise. But even here, in my judgment, the situation is not catastrophic; repairs will eventually be made, and the supply will be back on line in time. In the meantime, the higher oil prices (they may go as high as $4 a gallon) and the awe that all of us feel at the incredible destruction that Katrina has wrought will act to dampen our animal spirits a bit and cause a general slowing of the economy. I cannot emphasize enough, however, that the slowdown will be temporary. The rebuilding will give a big lift in the coming months.

The hypothetical situation above is neither a best case or a worst case scenario. The issues are far more complex for those people without insurance or are not able to maintain their jobs. In these cases, the burden falls to the state and federal governments. The costs will be terrific, but I believe all parties realize the magnitude of the problems and the consequences if any of them shirks their responsibilities. I am heartened that the state of Texas has not only offered the use of the Astro-Dome for the 25,000 refugees who were trapped in the Super-Dome, but has also opened their schools for the fall term to the school-age children who will living in the Dome.

I will report more on the rebuilding in time. The key thing for the economy is how long it takes to pump out the water and how long it takes to clean up the damage. From that point on, the economic benefits of the rebuilding will be substantial. Rebuilding the Delta region will take years, but the economy will be stronger than many commentators now believe.

The stock market is a discounting machine. It knows everything I have said here and more. I believe it will be able to look through Katrina's devastation and see that, in effect, she has slugged us, but our nation has proved over and over that we are resilient.

Addendum: Many are now saying that Katrina is the worst natural disaster in US history. The "Big Easy" has fallen, and she needs our help. I would encourage anyone reading this to contribute whatever you can to help those who have lost everything. Check with your local Red Cross. It is my understanding that they can take your contribution and get it to the Katrina relief effort.

Tuesday, August 23, 2005

Summer Stroll #18 - Retirement Respite

You have just retired. You have a million dollars to live on the rest of your life. Who do you trust to guide you? What do you put the money in? Where do you start? The old Who, What, Where questions bombard you with a weight that is surprising and unrelenting. You may be good at sales, or a whiz at accounting, fly a plane like nothing, or sing like a bird, but you are leaving your active career, and you are now faced with a job just as big and potentially more important that the job that produced this wealth. You are about to enter the world of Retirement Roulette. I keep using the term Roulette because unless you are very wise, you will do what most "financial planners" are recommending, and the moment you start down that road you are sowing the seeds of depleting your assets, if not literally, then figuratively. The reasons are two fold: 1. The annual fees of the financial planning crowd, which can run between 2% and 3%, are too high to permit investing in much fixed income securities. 2. This means that advisors who use only mutual funds must rely heavily on stock funds, whose volatility we believe many people in retirement find psychologically difficult to live with.

There is a way out of this game of chicken that is practical, doable, and livable. Let me go back to my idea of the buckets. In this case, I want to use the concept of what I will call the three buckets of retirement.

The first bucket will be invested in fixed income securities. Today it is possible to buy investment grade fixed income securities that yield near 6%. Let's say we have put half of our money in the fixed income bucket. At 6% it will produce annual income of about $30,000. This bucket will not grow, but its contents are safe and its principal and income will be very steady.

In bucket number two, we will invest in selected rising dividend stocks. The stocks we want in this bucket are stocks with as much dividend yield and dividend growth as we can find. Currently our Rising Dividend Model Portfolio yields 3.5%. That means if we invest the other half of our million dollars in bucket number two, we can expect to produce $17,500 in dividend income. Almost all of the companies in bucket number two have raised their dividends for years and possess strong finances so statistically we believe the odds are in the 90% range that this income will grow.

At this point, our portfolio will produce $47,500 in annual income. The first question you should ask is, "Why don't we put more money in bucket one? If we put it all in that bucket, we would have $60,000 in safe annual income."

Yes, you would but you would miss the rewards of bucket three. This bucket contains the price appreciation of the stocks in bucket two. Our Rising Dividend Portfolio has enjoyed annual dividend growth over many years of just over 7%. Indeed, over the past two years its dividend growth has been near 10%. But let's stick with 7% for the illustration. If dividend growth averages 7% over the next few years, we would expect the price appreciation of the portfolio to also grow by at least 7%. In addition, in most of the stocks in which we invest there is a high correlation (80%-90%) between dividend growth and price growth. Thus if we have the right stocks in bucket two, it is statistically a near certainty that we will achieve price growth in bucket three. Bottom line we expect bucket three will produce near $35,000 in average annual appreciation.

Our best guess is that the three bucket approach would produce $82,500 in average annual benefits. That's good news, but the best news is that only about 40% is in price appreciation. The other 60% would come from the income out of the other two buckets. Another good thing about the three bucket approach is that it is only approximately one-third to one-half as volatile as the standard asset allocation being recommended by many investment people today. Or said another way, it is an order of magnitude more predictable, thus livable.

We believe the secret to the three bucket approach is to keep expenses down by investing in individual stocks and bonds. In this way, we save the whole layer of fees that the mutual funds charge. We are money managers, and we charge a fee to manage accounts, but because we do not use mutual funds our total fees are a fraction of those that are routinely charged by the planning crowd. The money we save by cutting out the funds goes into our clients pockets. And because of our lower fees, we can invest in more income producing securities than can the typical recommended mutual fund asset allocation. Additionally, by investing in more income producing securities we can dramatically lower the volatility and risk.

There are of course all the usual disclaimers about trying to project the future by looking into the past, and there are questions that I have raised and not answered, but at the end of the day, your retirement years should not be a time when you are timing the market or supporting a financial planner's lifestyle, needlessly.

Ninty-nine percent of those of you who are reading this blog are probably clients or prospects of Donaldson Capital Management. If you are not, you owe it to yourself to see if an individually crafted three-bucket-investment plan would work for you.

My email is gdonaldson@dcmol.com. My phone number is 800-321-7442. Email me or call me. I'll get you in touch with one of our portfolio managers. It does not make any difference where you are. We have clients in 28 states. In the past week we have been in Arkansas, Alabama, Kentucky, Illinois, Tennessee, and Indiana.

We are harping on this not because we think we have the only answer, but judging from the new accounts that our firm is adding every day, the name brand investment firms in the Midwest do not have a clue about how to construct a portfolio that will stand the test of time and provide "Retirement Respite," instead of a Retirement Roulette.

Thursday, August 18, 2005

The Barnyard Forecast

Every day we get a new dose of economic data and depending upon the source(and political persuasion), of your news, you might conclude on some days that the the sky is falling, or on others that the sky's the limit. This is not a new phenomenon. We think it goes with the territory, so it is important to be able to zero in on just those few indicators that drive the markets. To provide a means of taking the pulse of the stock market's near-term prospects, many years ago we devised a very simple acronym, EIEIO, which helps us to focus our attention on the fewest and most important data points. Over time the acronym has become known as the Barnyard Forecast because EIEIO sounds like the chorus from the children's song, Old McDonald's Farm .

EIEIO is taken from the first letter of Economy, Inflation, Earnings, Interest Rates and Opportunity. Each of the indicators is scored on a three point scale for its positive or negative implications for stocks in the coming 6-12 months. We give each indicator 2 points if we believe the trend of the indicator is positive for the stock market, 1 point if it is neutral, and 0 points if it is negative.

Economy: The 80-year average of GDP is just over 3%, and we believe the ouch point for the Federal Reserve is 3.5% real growth. On a year over year basis, the GDP has grown at 3.6%. That is very good news for the economy, but not great news for the stock market because it means the Fed may well continue to raise short-term interest rates until the economy slows toward the 3-3.5% range. We rank the economy neutral for stocks, not because if its weakness, but because its strength will keep the Fed on the alert. 1 point.

Inflation: We believe the Fed's inflation ouch point is 2.5% on the core CPI. On a year over year basis, the core CPI has risen 2.6%. That's close enough to the acceptable level of 2.5% that we will give it a neutral score. 1 point.

Earnings: Earnings are nothing short of outstanding. Economy wide after-tax corporate earnings have risen nearly 20% in the last 12 months. That's good news anyway you look at it.

2 points.

Interest Rates: While the Fed has consistently pushed short rates higher, our model looks at 10-year bond yields and long-term mortgage rates. Both of these long-term interest rates are almost exactly where they were a year ago. We rate them neutral for stocks. 1 point.

Opportunity: Totaling the scores gives us a kind of short-hand view of the prospects for stocks in the next 6-12 months. At a total of 5 points (1+1+2+1) out of a total of 8 points, our model is suggesting a modestly positive rating for stocks.

We believe the Barnyard Forecast is suggesting the sideways motion of the major indices may continue at least until the Fed sees economic growth slow a bit. However, we continue to believe that companies with above average dividend yields and growth can escape this sideways motion. A stock with a 3% dividend yield and expected dividend growth of 7% offers an implied rate of return of 10%. With 10-year rates at 4.25%, these solid dividend payers are too cheap, and investors are increasingly recognizing it.

We will take a more in depth view of some the companies we like in the coming weeks.

Sunday, August 14, 2005

Summer Stroll #17 -- Retirement Roulette II

You've just been notified that you have a million dollars in retirement benefits. As we said in our last edition, that seems like a lot of money, but it will produce surprising little income in simple investments, maybe $35,000 - $40,000. With stocks having produced over 10% per annum over many years, it is natural in this low interest rate environment, that you would turn to stocks in hopes of producing a higher level of annual income. This seems simple enough, and from an expected return perspective, it is recommended for most people.