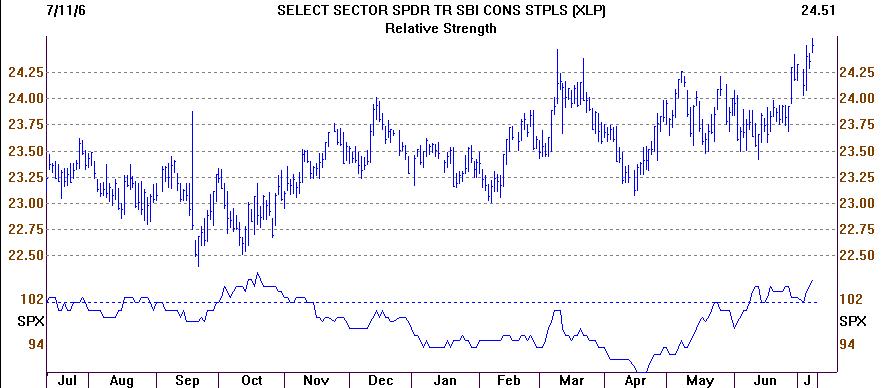

The chart is of the Dow Jones Select Dividend Index. This is collection of companies that meet specific requirements for dividend yield, dividend growth, and dividend payout. While this index is not a carbon copy of our Rising Dividend style of investing, it is comparable its industry mix and strategy.

The top of the chart shows the index's price graph over the last 12 months. The bottom of the chart shows the relative strength graph of the dividend index vs. the S&P 500 index. Both charts are eye popping.

The top graph shows that dividend-oriented stocks have broken out of a year-long trading range. Actually, the trading range was more like 18 months. The new 12 month high price for the dividend index may be a bit counter intuitive at first. There is a war in the Middle East, isn't their? Oil prices keep moving higher. Commodity prices keep moving higher. The Fed just raised rates for the umpteenth time. Everyone knows the mood on Wall Street is cool at best. Yet, in this "fog of war" and "fog of feelings" the dividend index has risen to a new high. This is important!!

In addition, the lower graph tells an even more interesting story. The graph shows that from about September of last year through April of this year, the dividend index consistently underperformed the S&P 500. At its nadir, the difference reached almost 7%. In my years in the business, I have seldom seen quality stocks so ignored -- shunned. I say quality stocks here because the dividend index, as constructed by Dow Jones, has a credit rating much higher than the average stock in the S&P 500.

But in April, things began to change and the dividend index began to show solid relative strength improvement, indicated by the graph turning up. The turn was sharp and strong but was interrupted by the Federal Reserves' tough talk and fears of inflation in June. The short downtrend changed directions again with the outbreak of the Middle East war. This time investors, in my mind, correctly saw that dividend-paying companies were a safer vehicle to ride out not only the fog of war, but also the slowing economy.

Now the dividend index has come all the way back to nearly catch the S&P Index for the year on a relative strength basis. To my way of thinking, the break out to a new high for the top graph (price) suggests that this pattern of outperformance by the dividend index will continue.

Our own model Rising Dividend Portfolio has had similar relative performance in the last three months versus the S&P 500 and has modestly outperformed the dividend index during this time on a median return basis.

In my judgment, a very big worm has turned, and big worms don't do much zig zagging, so I believe the swing back to high quality dividend-paying stocks will continue. They are cheap vs. growth-oriented stocks and now the momentum in in their favor. In the ways of Wall Street that is a tough combination to beat.

The chart is of the Dow Jones Select Dividend Index. This is collection of companies that meet specific requirements for dividend yield, dividend growth, and dividend payout. While this index is not a carbon copy of our Rising Dividend style of investing, it is comparable its industry mix and strategy.

The top of the chart shows the index's price graph over the last 12 months. The bottom of the chart shows the relative strength graph of the dividend index vs. the S&P 500 index. Both charts are eye popping.

The top graph shows that dividend-oriented stocks have broken out of a year-long trading range. Actually, the trading range was more like 18 months. The new 12 month high price for the dividend index may be a bit counter intuitive at first. There is a war in the Middle East, isn't their? Oil prices keep moving higher. Commodity prices keep moving higher. The Fed just raised rates for the umpteenth time. Everyone knows the mood on Wall Street is cool at best. Yet, in this "fog of war" and "fog of feelings" the dividend index has risen to a new high. This is important!!

In addition, the lower graph tells an even more interesting story. The graph shows that from about September of last year through April of this year, the dividend index consistently underperformed the S&P 500. At its nadir, the difference reached almost 7%. In my years in the business, I have seldom seen quality stocks so ignored -- shunned. I say quality stocks here because the dividend index, as constructed by Dow Jones, has a credit rating much higher than the average stock in the S&P 500.

But in April, things began to change and the dividend index began to show solid relative strength improvement, indicated by the graph turning up. The turn was sharp and strong but was interrupted by the Federal Reserves' tough talk and fears of inflation in June. The short downtrend changed directions again with the outbreak of the Middle East war. This time investors, in my mind, correctly saw that dividend-paying companies were a safer vehicle to ride out not only the fog of war, but also the slowing economy.

Now the dividend index has come all the way back to nearly catch the S&P Index for the year on a relative strength basis. To my way of thinking, the break out to a new high for the top graph (price) suggests that this pattern of outperformance by the dividend index will continue.

Our own model Rising Dividend Portfolio has had similar relative performance in the last three months versus the S&P 500 and has modestly outperformed the dividend index during this time on a median return basis.

In my judgment, a very big worm has turned, and big worms don't do much zig zagging, so I believe the swing back to high quality dividend-paying stocks will continue. They are cheap vs. growth-oriented stocks and now the momentum in in their favor. In the ways of Wall Street that is a tough combination to beat.

Enough said.