The chart at the right shows the S&P 500 price (red line, left axis) and earnings (blue line, right axis) on a simple two axis chart. The chart clearly shows, except for the Tech bubble of the late 1990s, that stock prices have tracked earnings very closely. The correlation is over 80%.

Please note that while stock prices were overly exuberant in the late 1990s, that they were too pessimistic in early 2009, falling much faster and farther than earnings did.

The arrow at the far right of the chart points to the current levels of S&P price and earnings. I have extended the earnings line (blue line) to reach current Wall Street earnings estimates for year end 2010. Analysts as of today are estimating that full-year 2010 earnings for the companies in the S&P 500 Index will reach just over $81. With current 12- month trailing earning standing at $69, that would mean that Wall Street expects strong earnings through the end of the year.

Additionally, if the analysts are correct and the historical relationship between prices and earnings reasserts itself by year end, the chart shows that the Index would be around 1400, much higher than its current level of about 1000.

It is clear that if history is to be our guide that both the bullish analysts and the bearish traders cannot both be right. We believe the time may be ripe for at least a partial resolution to the paradox. US companies will begin reporting second quarter earnings within the next ten days. If the analysts are wrong, we will know it very soon. We are inclined to think that their earnings estimates, if anything, will be low. If this were not the case, the financial press would have been full of companies announcing that they were going to miss their earnings targets. That has not happened, either.

Stocks fell sharply during the second quarter as the debt crisis in Greece, Portugal, and Spain became known. We believe the European Union has produced a bailout package for these countries that has a reasonable chance of working. There is some tough medicine in the form of spending cuts and wage adjustments. Nobody likes a pay cut, but we believe that is preferable to a fat check that bounces.

The times we live in are very fluid. The list of possible troubles is long. But there is one thing that many Americans don't seem to be able to put their arms around. One-third of the world's economic growth now comes from the developing nations of China, India, Brazil and the Far East. Not since the early 19th century has so much of the world GDP come from beyond the so-called developed countries.

We realize that we seem to be apologizing for the actions of the market a lot in recent months. We are not doing so out of blind faith. As a result of strong earnings growth over the last two quarters and falling stock prices, stocks have gotten very cheap by historical standards. Stocks are now trading about 13 times 2010 earnings, much lower than the 17 times geometric average P/E of the last 30 years.

The chart at the right shows the S&P 500 price (red line, left axis) and earnings (blue line, right axis) on a simple two axis chart. The chart clearly shows, except for the Tech bubble of the late 1990s, that stock prices have tracked earnings very closely. The correlation is over 80%.

Please note that while stock prices were overly exuberant in the late 1990s, that they were too pessimistic in early 2009, falling much faster and farther than earnings did.

The arrow at the far right of the chart points to the current levels of S&P price and earnings. I have extended the earnings line (blue line) to reach current Wall Street earnings estimates for year end 2010. Analysts as of today are estimating that full-year 2010 earnings for the companies in the S&P 500 Index will reach just over $81. With current 12- month trailing earning standing at $69, that would mean that Wall Street expects strong earnings through the end of the year.

Additionally, if the analysts are correct and the historical relationship between prices and earnings reasserts itself by year end, the chart shows that the Index would be around 1400, much higher than its current level of about 1000.

It is clear that if history is to be our guide that both the bullish analysts and the bearish traders cannot both be right. We believe the time may be ripe for at least a partial resolution to the paradox. US companies will begin reporting second quarter earnings within the next ten days. If the analysts are wrong, we will know it very soon. We are inclined to think that their earnings estimates, if anything, will be low. If this were not the case, the financial press would have been full of companies announcing that they were going to miss their earnings targets. That has not happened, either.

Stocks fell sharply during the second quarter as the debt crisis in Greece, Portugal, and Spain became known. We believe the European Union has produced a bailout package for these countries that has a reasonable chance of working. There is some tough medicine in the form of spending cuts and wage adjustments. Nobody likes a pay cut, but we believe that is preferable to a fat check that bounces.

The times we live in are very fluid. The list of possible troubles is long. But there is one thing that many Americans don't seem to be able to put their arms around. One-third of the world's economic growth now comes from the developing nations of China, India, Brazil and the Far East. Not since the early 19th century has so much of the world GDP come from beyond the so-called developed countries.

We realize that we seem to be apologizing for the actions of the market a lot in recent months. We are not doing so out of blind faith. As a result of strong earnings growth over the last two quarters and falling stock prices, stocks have gotten very cheap by historical standards. Stocks are now trading about 13 times 2010 earnings, much lower than the 17 times geometric average P/E of the last 30 years.

Wednesday, June 30, 2010

Paradox Found, May Be Soon Resolved

In recent weeks, the stock market seems to have lost it moorings and found itself thrashing about in heavy seas. US stocks appear to be caught in gale-force fears of all sorts of impending disasters from runaway inflation to a double dip in the economy.

But if the market's fears are justified, they should be showing up in the economic data. They are not. Indeed, the current level of core inflation on a year over year basis stands at 0.9%, the lowest annual figure since 1958. If anything this would tell us we should be worrying more about deflation than inflation. We can assure you that deflation is a greater worry than inflation to Ben Bernanke and his friends at the Federal Reserve. Furthermore, the economy is growing at just under 3%. That is slower than what we would expect coming out of the recent recession, but it is still close to the 50-year average annual GDP growth and shows good signs of continued modest growth.

If the recent sell off in stocks is justified, and not just the fear-induced selling by hedge funds and day traders, then we should expect to see analyst's earnings estimates collapsing. We don't see that either. Indeed, analyst earnings estimates for the S&P 500 Index continue to rise almost every week for year-end 2010.

If analysts are raising earnings estimates while stock prices are falling, it would mean that the market does not believe the earnings are sustainable and may fall apart in 2011. But the analysts are not just hiking estimates for the next six months, they are also hiking earnings estimates for 2011. As of today the consensus estimate for the S&P 500 is that earnings will grow by nearly 17% in 2011. If the analysts are to be believed, then the current selling price of the S&P 500 is way under priced.

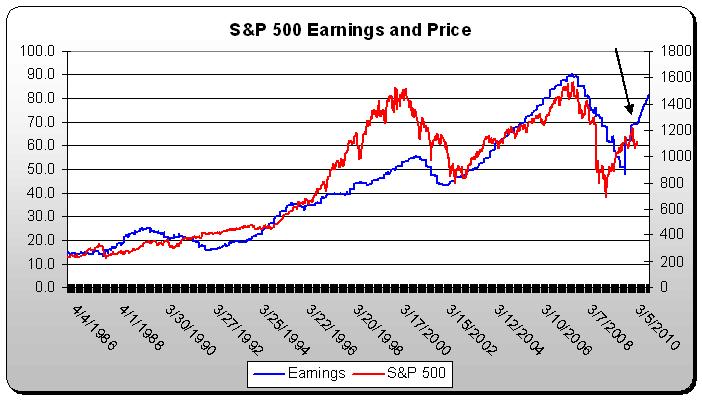

Click the chart to enlarge. The chart at the right shows the S&P 500 price (red line, left axis) and earnings (blue line, right axis) on a simple two axis chart. The chart clearly shows, except for the Tech bubble of the late 1990s, that stock prices have tracked earnings very closely. The correlation is over 80%.

Please note that while stock prices were overly exuberant in the late 1990s, that they were too pessimistic in early 2009, falling much faster and farther than earnings did.

The arrow at the far right of the chart points to the current levels of S&P price and earnings. I have extended the earnings line (blue line) to reach current Wall Street earnings estimates for year end 2010. Analysts as of today are estimating that full-year 2010 earnings for the companies in the S&P 500 Index will reach just over $81. With current 12- month trailing earning standing at $69, that would mean that Wall Street expects strong earnings through the end of the year.

Additionally, if the analysts are correct and the historical relationship between prices and earnings reasserts itself by year end, the chart shows that the Index would be around 1400, much higher than its current level of about 1000.

It is clear that if history is to be our guide that both the bullish analysts and the bearish traders cannot both be right. We believe the time may be ripe for at least a partial resolution to the paradox. US companies will begin reporting second quarter earnings within the next ten days. If the analysts are wrong, we will know it very soon. We are inclined to think that their earnings estimates, if anything, will be low. If this were not the case, the financial press would have been full of companies announcing that they were going to miss their earnings targets. That has not happened, either.

Stocks fell sharply during the second quarter as the debt crisis in Greece, Portugal, and Spain became known. We believe the European Union has produced a bailout package for these countries that has a reasonable chance of working. There is some tough medicine in the form of spending cuts and wage adjustments. Nobody likes a pay cut, but we believe that is preferable to a fat check that bounces.

The times we live in are very fluid. The list of possible troubles is long. But there is one thing that many Americans don't seem to be able to put their arms around. One-third of the world's economic growth now comes from the developing nations of China, India, Brazil and the Far East. Not since the early 19th century has so much of the world GDP come from beyond the so-called developed countries.

We realize that we seem to be apologizing for the actions of the market a lot in recent months. We are not doing so out of blind faith. As a result of strong earnings growth over the last two quarters and falling stock prices, stocks have gotten very cheap by historical standards. Stocks are now trading about 13 times 2010 earnings, much lower than the 17 times geometric average P/E of the last 30 years.

The chart at the right shows the S&P 500 price (red line, left axis) and earnings (blue line, right axis) on a simple two axis chart. The chart clearly shows, except for the Tech bubble of the late 1990s, that stock prices have tracked earnings very closely. The correlation is over 80%.

Please note that while stock prices were overly exuberant in the late 1990s, that they were too pessimistic in early 2009, falling much faster and farther than earnings did.

The arrow at the far right of the chart points to the current levels of S&P price and earnings. I have extended the earnings line (blue line) to reach current Wall Street earnings estimates for year end 2010. Analysts as of today are estimating that full-year 2010 earnings for the companies in the S&P 500 Index will reach just over $81. With current 12- month trailing earning standing at $69, that would mean that Wall Street expects strong earnings through the end of the year.

Additionally, if the analysts are correct and the historical relationship between prices and earnings reasserts itself by year end, the chart shows that the Index would be around 1400, much higher than its current level of about 1000.

It is clear that if history is to be our guide that both the bullish analysts and the bearish traders cannot both be right. We believe the time may be ripe for at least a partial resolution to the paradox. US companies will begin reporting second quarter earnings within the next ten days. If the analysts are wrong, we will know it very soon. We are inclined to think that their earnings estimates, if anything, will be low. If this were not the case, the financial press would have been full of companies announcing that they were going to miss their earnings targets. That has not happened, either.

Stocks fell sharply during the second quarter as the debt crisis in Greece, Portugal, and Spain became known. We believe the European Union has produced a bailout package for these countries that has a reasonable chance of working. There is some tough medicine in the form of spending cuts and wage adjustments. Nobody likes a pay cut, but we believe that is preferable to a fat check that bounces.

The times we live in are very fluid. The list of possible troubles is long. But there is one thing that many Americans don't seem to be able to put their arms around. One-third of the world's economic growth now comes from the developing nations of China, India, Brazil and the Far East. Not since the early 19th century has so much of the world GDP come from beyond the so-called developed countries.

We realize that we seem to be apologizing for the actions of the market a lot in recent months. We are not doing so out of blind faith. As a result of strong earnings growth over the last two quarters and falling stock prices, stocks have gotten very cheap by historical standards. Stocks are now trading about 13 times 2010 earnings, much lower than the 17 times geometric average P/E of the last 30 years.

The chart at the right shows the S&P 500 price (red line, left axis) and earnings (blue line, right axis) on a simple two axis chart. The chart clearly shows, except for the Tech bubble of the late 1990s, that stock prices have tracked earnings very closely. The correlation is over 80%.

Please note that while stock prices were overly exuberant in the late 1990s, that they were too pessimistic in early 2009, falling much faster and farther than earnings did.

The arrow at the far right of the chart points to the current levels of S&P price and earnings. I have extended the earnings line (blue line) to reach current Wall Street earnings estimates for year end 2010. Analysts as of today are estimating that full-year 2010 earnings for the companies in the S&P 500 Index will reach just over $81. With current 12- month trailing earning standing at $69, that would mean that Wall Street expects strong earnings through the end of the year.

Additionally, if the analysts are correct and the historical relationship between prices and earnings reasserts itself by year end, the chart shows that the Index would be around 1400, much higher than its current level of about 1000.

It is clear that if history is to be our guide that both the bullish analysts and the bearish traders cannot both be right. We believe the time may be ripe for at least a partial resolution to the paradox. US companies will begin reporting second quarter earnings within the next ten days. If the analysts are wrong, we will know it very soon. We are inclined to think that their earnings estimates, if anything, will be low. If this were not the case, the financial press would have been full of companies announcing that they were going to miss their earnings targets. That has not happened, either.

Stocks fell sharply during the second quarter as the debt crisis in Greece, Portugal, and Spain became known. We believe the European Union has produced a bailout package for these countries that has a reasonable chance of working. There is some tough medicine in the form of spending cuts and wage adjustments. Nobody likes a pay cut, but we believe that is preferable to a fat check that bounces.

The times we live in are very fluid. The list of possible troubles is long. But there is one thing that many Americans don't seem to be able to put their arms around. One-third of the world's economic growth now comes from the developing nations of China, India, Brazil and the Far East. Not since the early 19th century has so much of the world GDP come from beyond the so-called developed countries.

We realize that we seem to be apologizing for the actions of the market a lot in recent months. We are not doing so out of blind faith. As a result of strong earnings growth over the last two quarters and falling stock prices, stocks have gotten very cheap by historical standards. Stocks are now trading about 13 times 2010 earnings, much lower than the 17 times geometric average P/E of the last 30 years.

Thursday, June 24, 2010

Soccer Coach Yeagley's Contribution to Our Investment Strategy

I am a soccer fan, therefore I am aglow with pride over the USA's victory over Algeria to win their group phase in the World Cup in South Africa.

My love for "football" came because both of my sons gave up playing my sports (baseball and basketball) when they were very young to concentrate on soccer. Since I love both of my sons, perhaps it was only natural that I would come to love the game they loved, even though for many years I did not understand the difference between a "corner kick" and a "free kick."

My understanding of the game bloomed as a result of my younger son, Nick, being recruited by legendary Indiana University coach, Jerry Yeagley. Our family started driving to Bloomington, Indiana, every chance we got to watch Yeagley's Indiana team demolish their opponents. Yeagley would ultimately win 6 national championships during his 30+ years as coach of the Hoosiers.

Nick ultimately matriculated to IU to play for coach Yeagley. He learned after a few days of practice that he was to be red-shirted, which meant that he would not appear in any games in his freshman year. That was a disappointment to Nick and our family but there was a bit of sugar with the lemon. Every Wednesday night at practice, there was a full scrimmage between the first team and the second team, which consisted of many red-shirt players.

I began a weekly pilgrimage to Armstrong Stadium in Bloomington to watch these highly competitive, entertaining scrimmages and a chance to watch Nick show his stuff. Many other parents also came to these matches because the team was large and the playing time small.

I also began making the two hour drive each week because being in the investment business, I'm always interested in winners: Who they are? How did they get that way? I was delighted that Coach Yeagley was always very open in his explanations of why he believed his Hoosiers had been such consistent winners.

Among the basics he mentioned were that speed trumped skill and that conditioning trumped speed. Furthermore defense trumped offense, and that defense was a function of conditioning and teamwork.

He surprised me one day when he said that when he was recruiting a young man, his first visit was to his guidance counselor. He wanted to know what kind of person the young man was away from soccer. Did he care about grades or his teachers and fellow students. I asked coach why this was so important. He said that in the IU program defense was key and defense took speed and conditioning, but defense also was a function of teamwork.

A team might have one big-time scorer, but there was no such thing as a solo big-time defender. Defense was completely a function of teamwork and organization. If the young man was a prima dona or a head case, he would never be able to endure the tough conditioning and teamwork drills that were at the core of IU's program.

Coach Yeagley told me one evening that he had sought out IU basketball coach, Bobby Knight, to learn about his coaching philosophy. Not surprisingly coach Yeagley said that he had adapted some of coach Knights defensive theories into his own approach to soccer.

Coach Yeagley said skill was necessary for winning, but that a team could get by on far less skill than most coaches thought. Three or four highly skilled players could produce scoring, but it took eleven men to defend properly. I remember one of his great teams had three back line defenders who were not recruited by any colleges to play soccer. They had all been outstanding Indiana high school basketball players but were only above average soccer players when they came to IU. Coach reasoned that if a kid was fast enough and knew the principles of playing man to man defense in basketball that he could teach him to play a smothering defense in soccer.

Let me bring this story around to investing. I don't' think I ever thanked Coach Yeagley for something he taught me about investing. Actually it was something he said about winning soccer that suddenly rang true about winning investing.

He said there are four periods of a game when most scoring occurs: in the first five minutes of the first and second halves and in the last five minutes of the first and second halves. Scoring often comes during the first five minutes of each half because one or both teams is not organized -- a failure of teamwork. Scoring often comes at the end of the first and second halves because of fatigue. The average midfield soccer player runs nearly five miles during a match. Since players are seldom substituted in soccer, at the ends of both halves, fatigue is burning in the lungs and legs of every man on the field. Not only that, but fatigue also drains the will to win.

He said IU had a history of scoring during these five minutes periods, not so much because of what they did, but because of what the other teams did not do. He said that it was his intention that no team be in better condition than IU, but just in case they were, that the scrimmage on Wednesday night showed each starter just how many guys were after his job and just how close they were.

I took away from those conversations with Coach Yeagley a realization that I have repeated ad nauseum. At Donaldson Capital Management we own companies that can last. Our companies possess the financial strength and corporate strategies that can last through recessions, periods of inflation, stagflation, booms, busts, and even from time to time inept corporate management. We attempt to own companies that are financially fit, good team players, good citizens, and know how to win, fairly and squarely. Teams that never give up and always believe that time is on their side.

Interestingly, the USA's soccer team has scored twice as many goals in the last five minutes of their matches as any other team in the tournament over the last four years. Somewhere in Bloomington Indiana Coach Jerry Yeagley is surely smiling.

Go USA, beat Ghana.

Friday, June 18, 2010

Ten Quick Facts about Dividends for the S&P 500

Dividends are alive and well and getting back to normal. At least that is what the data for the first six months of the year would indicate. The following is a brief update on the dividend actions or inaction's of the 500 companies in the Standard and Poors Index for calendar year 2010.

This information is based on announced dividend actions as reported by Bloomberg and is taken from Bloomberg Professional Data.

- 361 pay a dividend.

- 139 do not pay a dividend.

- 3 have cut or eliminated their dividends in 2010.

- 12 have initiated or reinstated their dividends.

- 97 have announced a dividend increase.

- The median increase for those companies hiking their dividend has been 6%.

- The industries with the most dividend increases have been the Consumer Cyclicals and the Industrials.

- Almost all major banks have kept their dividends stable. They appear to be under government orders to do so.

- The most surprising dividend hike was Target's nearly 50% increase.

- Dividend income for the S&P 500 companies is on track to increase on a year over year basis for the first time since 2007.

Dividend taxes may be going up, but corporations show no signs of opting for share buybacks as opposed to dividend hikes. With US corporations literally rolling in cash flows, we expect more dividend hikes over the remainder of the year.

Target is held by some principals and clients of DCM.

Friday, June 04, 2010

Bad News for Jobs: Small Businesses Have Dug in Their Heels

Anyway you look at it, the jobs report released Friday was flat ugly. Almost all the new jobs created were government census workers. Even though the unemployment rate ticked lower to 9.8%, the lack of new jobs in the private sector was an unpleasant surprise to economists and stock traders. Stocks fell sharply and bond prices rallied.

We believe the stock market's reaction to the news is overdone, but it is clear that the US economy is still limping along and, thus, employers remain very reluctant to add new jobs. Indeed, if you look at job growth over the last decade no one should be surprised at the weak US job data.

According to economist, Ed Yardeni, since 2001 nearly 90% of all new jobs have been created by small businesses. So, if you want to know why job growth is so paltry, you only have to consider the current mind-set of small businesses. It is not a pretty sight.

Small businesses will take a direct hit from the increased costs associated with the Obama administration's government health-care and financial reforms. In addition, many small business people will take the full body blow of the tax increases that the president and his Democratic colleagues have proposed. Finally, consider that as a result of the increased scrutiny of banks by federal regulators that it is now more difficult for small businesses to get bank loans for expansion.

When you put it all together, it becomes clear why small businesses don't feel particularly optimistic about the future, and why, in the current political and business environment, that their attitude is not likely to change. This pessimism is made worse as small business people watch as industry after industry is hauled in before Congressional inquisitions and accused of being a scourge on society.

The question we hear over and over from our small business clients is, "Where is this all going to end?"

While small businesses are taking their lumps, we believe that larger companies are thriving. The reason is simple, the world economy is growing faster than the US economy. The developing nations of the world are growing two or three times as fast as the developed world. Large multi-national companies, by their very nature, are taking advantage of this world wide growth. Additionally, they have access to the capital markets, which means they are not reliant on the banks to fund their growth. Finally, they have corporate staffs to sort out and attempt to understand the thousands of pages of new regulations that are coming out of Washington.

As we have written in previous blogs, we are optimistic that large corporations will continue to show very strong earnings growth. As long as this trend continues, we believe stock prices will eventually calm down and begin to follow the rising trend of higher earnings.

Tuesday, June 01, 2010

Here's Why We Think Stocks Will Rise

At our Investment Policy Committee meeting today our discussion focused mainly on three topics.

1) Is the risk discount built into current stock prices excessive?

2) How tightly is the US economy tied to Europe? and

3) How tied are the companies we invest in to either the US or European economies?

1) The Committee believes that by almost any traditional measure, today’s stock market (S&P 500) is significantly underpriced. Current estimates of 2010 and 2011 corporate earnings have held at their current high levels for weeks – right through the Greek debt crisis, China economic slowdown fears, Korean conflicts, volcanic ash-induced slowdown of European commerce, etc., etc.

In addition, Q1 earnings exceeded analysts’ estimates by a near record level. In fact, total corporate profits for the entire US economy on a rolling 12 month basis as of 03/31/10 were just 6% below their record high in Q3 2006. Finally, employment costs, inflation, and interest rates are low and unlikely to increase much this year, adding up to a very favorable earnings environment.

Using almost any traditional measure of stock market valuation, the market is undervalued. Using the “Fed Model” (Est Future Earnings/ Current Stock Price = Yield on 10-yr Treasury Note) the S&P should now be at 2562 vs. its actual level of 1085 – a 57% discount!

It’s reasonable to argue these are exceptional times, especially for Treasury yields. With the world fleeing European debt and buying US debt, Treasury yields are exceptionally low. So, to be exceptionally conservative, we could use a more “normal” 10-yr yield of 5% instead of the current 3.3% and we could use low historical earnings instead of high estimated future earnings. Even with that calculation, the market should be 20% higher, or about 1296. ( DCM has previously estimated 12/31/10 S&P 500 to be between 1200 – 1300.)

Today’s market valuation is low primarily due to perceived risk, not low projected profits. That risk has mostly come from fears that the Greek debt crisis would pull down Europe, and then the rest of the world. Europe has definite problems, but the recent $1 trillion bailout we believe has successfully bought a few years of time to fix them. Therefore, we believe the current “risk discount” for US stocks is overdone and is more due to a holdover of fear and anxiety from the 2008 – 2009 experience.

Once the world sees that Europe is not going to collapse, we fully expect market valuations to edge back up toward the historical norm.

2) We have previously discussed estimates that 25% of U.S. corporate earnings comes from Europe. New data from the Bureau of Economic Analysis estimates that now only 20% of U.S. earnings come from exports to Europe. Two observations, the estimates are getting lower, not higher. And, both are in the 20% - 25% range. Europe has been losing significance to US multi-national companies for a few years because growth has been so scarce in Europe. Twenty percent of sales and earning is not insignificant, but even if Europe has more trouble than we now forecast, sales and earnings aren't going to zero, thus we believe the US stock market is overreacting to the goings on in Europe.

3) We have long said that we don’t invest in economies. We invest in companies. The data on corporate earnings discussed earlier show that U.S. companies in total are expecting to increase earnings dramatically in 2010 over 2009, and as much as 20% again in 2011. An estimated 60% of U.S. exports goes to developing economies like China, India, and Brazil. Each of these countries is expecting near double-digit GDP growth this year.

Even for the Rising Dividend companies that do not have large export businesses (mostly the banks and utilities) overall economic growth does not necessarily dictate individual company growth. In fact, even in the terrible economy of 2008 – 2009, there were still winners, both relative and absolute. Since we choose Rising Dividend companies in part based on their proven success at outperforming competitors, we believe that many, if not most, of our companies will do well even if the world GDP grows more slowly than we expect this year.

Most large companies these days really are more global than domestic. Many derive far less than ½ of their business from inside the U.S. We believe that gives them a greater opportunity to grow earnings at a much faster rate than the economies of any of the developed nations of the world.

Back to #1, we observed that institutional investors (think big investment banks, brokerage houses, etc.) now represent 70% of market volume, double the 35% they represented in 1975. And, we have seen statistics that claim on a given day, high-speed, computer–driven trading, alone, can be 70% of total volume. That means on many days, market prices are determined by very short term (even nanosecond) factors, not long-term fundamentals. Since this short-term trading tends to accentuate, not reduce momentum, then up days go higher and down days go lower than if the day to day market prices were determined by investors buying a stock to hold for years…or even months.

This short-term trading certainly adds to volatility, but it cannot indefinitely hold back the stock prices of companies that truly increase value for customers year after year.

For many of the stocks we hold, the correlation between dividend growth and price growth is over 80%. The price growth does not come in a tit-for-tat basis but "equalizes" about every two to three years. We see countless valuation charts that indicate many of the companies we hold are undervalued in the range of 30%-40%.

In the past 3 months, 9 Cornerstone model companies increased their dividend by an average of nearly 9%. The value creation continues.

In short, the Committee continues to believe that earnings and dividend growth will ultimately win the day (as they always have), and the market will push to much higher levels. The unanimous feeling among our 5 portfolio managers was that it is a great time to buy great companies at great prices.

Sources: briefing.com; Yardeni.com; and, Bloomberg

Subscribe to:

Posts (Atom)