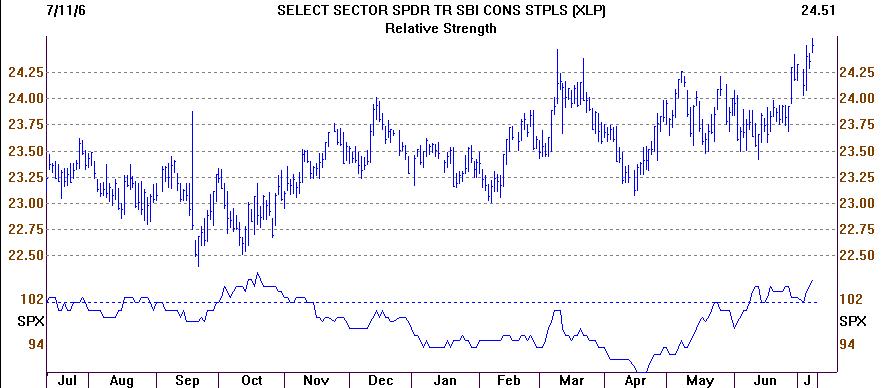

The chart shows that the price trend (the top graph) has broken out of year-long sideways movement to hit a new intermediate high. In addition, the lower chart, which shows the relative strength of the consumer staples vs. the S&P 500, also shows a upside breakout. This double breakout is a very good sign that the staples are signaling a move to even higher ground.

Our valuation work shows that while this sector's financial strength rating is amongst the highest of all sector ratings, it is one of the most undervalued sectors in the current market. Timing is a tricky thing in the market, but it would appear that the valuation gap for the staples sector is beginning to close. I'll keep you updated from time to time on its progress.

The chart shows that the price trend (the top graph) has broken out of year-long sideways movement to hit a new intermediate high. In addition, the lower chart, which shows the relative strength of the consumer staples vs. the S&P 500, also shows a upside breakout. This double breakout is a very good sign that the staples are signaling a move to even higher ground.

Our valuation work shows that while this sector's financial strength rating is amongst the highest of all sector ratings, it is one of the most undervalued sectors in the current market. Timing is a tricky thing in the market, but it would appear that the valuation gap for the staples sector is beginning to close. I'll keep you updated from time to time on its progress.

Tuesday, July 11, 2006

The Consumer Staples Sector Comes to Life -- More to Follow

I have been saying for nearly a year that quality was being undervalued by the market. By that I have meant companies with AA and AAA financial strength ratings and solid earnings have been priced like East Pearidge Sand and Gravel. Indeed, I have commented to many people my amazement at the fact that nearly all of the high quality multinational growth stocks have been trading at a PE of near 20, about the same as the average small cap stock, whose fortunes are not nearly so established or predictable.

I have concluded that lack of appreciation for and consequent lack of price appreciation in the great blue chip growth stocks was because of the strong economy and the lack of concern about risk. In this kind of environment, Wall Street will often move to smaller companies whose prospects are not so predictable, hoping to get lucky, so to speak. In recent blogs and client letters, I have explained that as the Fed continues to push rates higher, risk will soon become much more important. The reason is simple: the higher rates will slow the economy, and the slowing economy will impact earnings. The companies whose earnings will be impacted the most are those companies most directly tied to the US economy -- small and mid cap companies.

High-quality, multinational companies derive as much as 70% of their earnings outside the US. Additionally, their businesses are much more apt to be what I call necessary services -- consumer staples, healthcare, energy, and financial services -- all less sensitive to the economy that lower quality companies.

I believe the first evidence of this is now occurring. The chart below is of the S&P Consumer Staples. The staples, which include Coke, Pepsi, Procter and Gamble, Colgate, Walmart and many more, have been laggards for the past couple of years. In recent weeks in the face of thought talk by the Fed, that underperformance has turned abruptly and convincingly.

Click to enlarge**

The chart shows that the price trend (the top graph) has broken out of year-long sideways movement to hit a new intermediate high. In addition, the lower chart, which shows the relative strength of the consumer staples vs. the S&P 500, also shows a upside breakout. This double breakout is a very good sign that the staples are signaling a move to even higher ground.

Our valuation work shows that while this sector's financial strength rating is amongst the highest of all sector ratings, it is one of the most undervalued sectors in the current market. Timing is a tricky thing in the market, but it would appear that the valuation gap for the staples sector is beginning to close. I'll keep you updated from time to time on its progress.

The chart shows that the price trend (the top graph) has broken out of year-long sideways movement to hit a new intermediate high. In addition, the lower chart, which shows the relative strength of the consumer staples vs. the S&P 500, also shows a upside breakout. This double breakout is a very good sign that the staples are signaling a move to even higher ground.

Our valuation work shows that while this sector's financial strength rating is amongst the highest of all sector ratings, it is one of the most undervalued sectors in the current market. Timing is a tricky thing in the market, but it would appear that the valuation gap for the staples sector is beginning to close. I'll keep you updated from time to time on its progress.

The chart shows that the price trend (the top graph) has broken out of year-long sideways movement to hit a new intermediate high. In addition, the lower chart, which shows the relative strength of the consumer staples vs. the S&P 500, also shows a upside breakout. This double breakout is a very good sign that the staples are signaling a move to even higher ground.

Our valuation work shows that while this sector's financial strength rating is amongst the highest of all sector ratings, it is one of the most undervalued sectors in the current market. Timing is a tricky thing in the market, but it would appear that the valuation gap for the staples sector is beginning to close. I'll keep you updated from time to time on its progress.