There are two graphs on the chart. The green (dark) line is nominal or headline CPI, which measures the actual rate of inflation, and the brown (light) line is the "core" CPI, which excludes food and energy from nominal CPI. The core CPI is what most economists watch because food and energy are very volatile and can distort the data when viewed too narrowly. Chart I shows that the nominal CPI has been on a steady march higher since the end of 2001. Core CPI has been much steadier, spending most of it time between 1.5% and 2.5% over the last 9 years.

Interestingly, the 80 year average of both indices is near 3%, and this is the reason that the Fed and most economists pay more attention to the core rate of inflation. It is less volatile than the nominal CPI and, in the long run, it has increased at the same rate.

Yesterday almost $200 billion was chopped from the value of the S&P 500 because both measures of inflation were slightly higher than forecasts. The nominal CPI was .6% for April and the core CPI was up .3%. Most experts expected nominal CPI to be a big number because oil prices had risen nearly $5 per barrel in April but forecasted that the core CPI would come in at .2%. So in a manner of speaking a .1% miss on the core CPI was worth about $200 billion in stock values.

The reason the stock market reacted so negatively can be understood by looking again at ChartI. The core CPI has gone sideways at near 2% annual growth for the last year. It has done so in the face of a big increase in oil prices and some food commodities, and the effects of Katrina, et al. The problem is the .3% increase in the core CPI for the month of April has now turned the nose of core CPI up. If core CPI is, indeed, moving higher, then the Fed will continue to push rates higher and the recent rally in stocks will stall. The reason is simple: even though first quarter earnings have been outstanding, at least some of the rally in recent weeks, has been based on the notion that the Fed was nearing completion of its rate hikes.

I am not in the camp that believes that the Fed has a lot of work left to do, and the reason can be seen in Chart II.

There are two graphs on the chart. The green (dark) line is nominal or headline CPI, which measures the actual rate of inflation, and the brown (light) line is the "core" CPI, which excludes food and energy from nominal CPI. The core CPI is what most economists watch because food and energy are very volatile and can distort the data when viewed too narrowly. Chart I shows that the nominal CPI has been on a steady march higher since the end of 2001. Core CPI has been much steadier, spending most of it time between 1.5% and 2.5% over the last 9 years.

Interestingly, the 80 year average of both indices is near 3%, and this is the reason that the Fed and most economists pay more attention to the core rate of inflation. It is less volatile than the nominal CPI and, in the long run, it has increased at the same rate.

Yesterday almost $200 billion was chopped from the value of the S&P 500 because both measures of inflation were slightly higher than forecasts. The nominal CPI was .6% for April and the core CPI was up .3%. Most experts expected nominal CPI to be a big number because oil prices had risen nearly $5 per barrel in April but forecasted that the core CPI would come in at .2%. So in a manner of speaking a .1% miss on the core CPI was worth about $200 billion in stock values.

The reason the stock market reacted so negatively can be understood by looking again at ChartI. The core CPI has gone sideways at near 2% annual growth for the last year. It has done so in the face of a big increase in oil prices and some food commodities, and the effects of Katrina, et al. The problem is the .3% increase in the core CPI for the month of April has now turned the nose of core CPI up. If core CPI is, indeed, moving higher, then the Fed will continue to push rates higher and the recent rally in stocks will stall. The reason is simple: even though first quarter earnings have been outstanding, at least some of the rally in recent weeks, has been based on the notion that the Fed was nearing completion of its rate hikes.

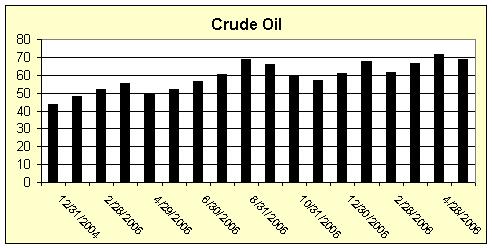

I am not in the camp that believes that the Fed has a lot of work left to do, and the reason can be seen in Chart II.

Chart II shows the monthly price of crude oil since 12/31/04. The most recent three bars of the data are the key drivers of the inflation story in the short run. The last bar on the right hand side of the chart shows today's price for oil of $68.80 per barrel. The data that was released yesterday reflected the nearly $5 per barrel run up in the price of oil for the month of April, which ended the month at $71.9. Since the end of April, prices have fallen about $3 per barrel. If this price decline holds through the end of the month, May's CPI data will be much lower than the just-reported numbers for April.

Chart II shows the monthly price of crude oil since 12/31/04. The most recent three bars of the data are the key drivers of the inflation story in the short run. The last bar on the right hand side of the chart shows today's price for oil of $68.80 per barrel. The data that was released yesterday reflected the nearly $5 per barrel run up in the price of oil for the month of April, which ended the month at $71.9. Since the end of April, prices have fallen about $3 per barrel. If this price decline holds through the end of the month, May's CPI data will be much lower than the just-reported numbers for April.

But, even if oil prices stay high, I believe inflation will stabilize and begin to fall in the months ahead for three very big reasons: (1) It is well known that Fed rate actions work with a lag of 6-12 months. Thus, the effects of their recent hikes have not yet been felt by the economy. (2) There is little doubt that the hot real estate market is cooling. A slowing real estate market will slow the economy and diminish price increases in housing related raw materials, which have been rising sharply in recent years. (3) The effects of higher oil prices, while affecting inflation, also impact economic growth. The reason is simple: higher energy prices come right out of consumer's pocket books, leaving them less money for other discretionary spending.

Additionally, substitution is starting to take place. As I write this letter the CEOs of the major auto manufacturers are in Washington DC lobbying for more filling stations across America capable of pumping grain-based alternative fuels. There is, obviously, a lot of politics in the promotion of alternative fuels, but, in my judgment, it has now become clear to leaders of all stripes that our country cannot continue its dependence solely on oil rationed to us by countries who are our enemies.

One sign that things are changing was the recent announcement by Archer-Daniel-Midland that they had hired a former Chevron executive as their new CEO. ADM is the leading player in the ethanol alternative fuels market and giving its top job to an oil executive is not a publicity stunt. They see a change in the winds and they are moving to capitalize on it.

Other anecdotal evidence that consumers are changing their buying habits is news that big SUVs are not selling well, and that high mileage used cars are bringing remarkable prices. CNN reports that a year old Toyota Prius is now fetching a higher price than when it was new, even with 20,000 miles.

Inflation concerns will continue to be the driver of both stocks and bonds until nominal CPI falls below 3%. And, while I am not claiming that inflation is whipped, a final look at Chart I shows that, even with the recent bad CPI data for the month of April, nominal CPI appears to have peaked and is now trending lower. Couple this with the falling oil prices in recent weeks and the inflation picture becomes a lot brighter.

Finally, even factoring in higher interest rates, our valuation model for the blue chip indices are suggesting that stocks are underpriced.

I will continue with the third call from Black Monday 1987 soon.