Monday, January 09, 2006

Stocks are Very Cheap

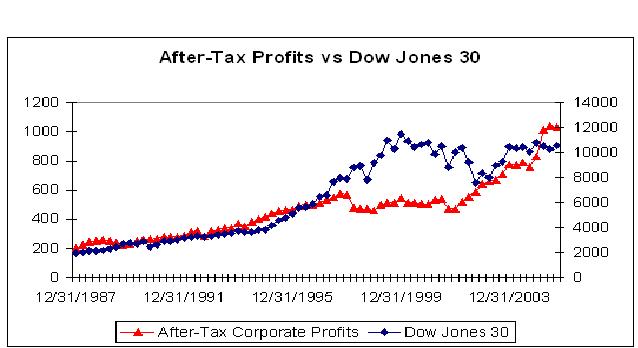

The chart below shows total US after-tax corporate profits versus the price of the Dow Jones Industrial Average since the beginning of 1988. You will notice that the two moved in tandem from 1988 through 1996. At that point, they diverged with the Dow going up and profits going down. Even when you say this out loud, something does not sound right -- stock prices started moving higher while profits were going down? That divergence lasted until 2003, when prices and profits once again converged. I have shown this chart before, and I think it explains a lot about the markets in general and the market today in particular.

The markets are not as efficient as the professors would have us believe. They get over valued and undervalued, and can stay that way for much longer than would seem appropriate. I actually knew about this data in the mid 1990s and convinced myself that the divergence in prices and profits was justified by the fall in inflation and interest rates. I was wrong. As it turns out, the market operates pretty much like we all thought -- it stumbles around, gets lost, zigs when it should be zagging, and yet thank goodness, sometimes, it gets it right. In my judgment, we are entering a period when it will get it right.

The chart shows that after-tax corporate profits have been very strong. Before we go any farther consider that these are the profits corporations are willing to pay taxes on; need I say anything further about their authenticity? Profits have been accelerating and have now moved decisively above the very flat line for stock prices. This is my point: with the expected 8%-10% growth in profits for 2006, the profit line will be equivalent to about 13,000 on the Dow Jones Industrial Average.

More Later,