Saturday, March 25, 2006

Conagra -- Able, Willing, and Ready -- Not

Thursday, March 16, 2006

In the Long run, Price Follow Dividends -- Part II

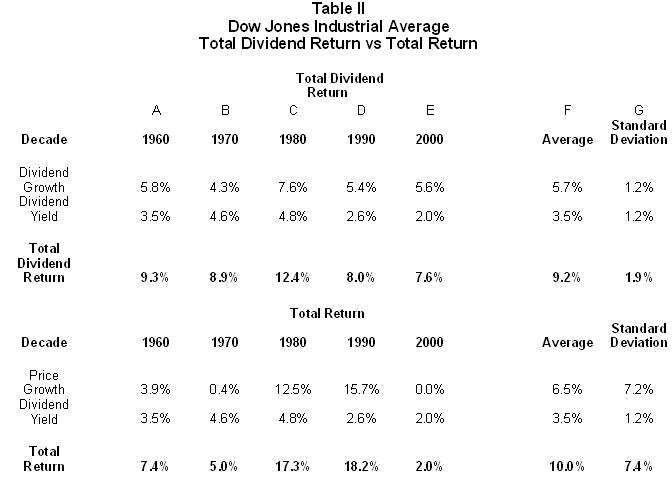

Table II has a lot going on, so let us describe the major points we will be discussing. The table shows the rates of returns for prices and dividends and the variability of the returns over the last five decades of the Dow Jones Industrial Average. The table compares the well-known concept of investment total return with our less well known “Total Dividend Return.” Our purpose in showing this table is to complete our discussion of a point we brought up earlier about dividends. We said the following:

“Importantly, our research shows that in the case of the DJIA, the steadily rising dividends have not only increased the investment returns they have also provided an important indication of the valuation of the DJIA itself. . . .”

At Donaldson Capital Management, we often say that many of our companies’ dividends are consistent and persistent. Just how consistent they are may surprise you. Earlier we said that the cumulative dividends of the DJIA have risen about 8 out every 10 years. The upper half of Table II shows dividend growth and dividend yield over the last five decades. Column A shows in the 1960s dividends grew by an average of 5.8% per year. Column F reveals that the average dividend growth for the last five decades has been 5.7%. The chart vividly shows that dividend growth has been very consistent during this time, with only the 7.6% growth in 1980s diverging very far from the growth of the other decades. We investigated this divergence and found that it was driven by the large dividend increases that companies made in 1987 and 1988. This was in the aftermath of the stock market crash in 1987, and we believe the outsized increases were the DJIA companies’ attempt to reassure their shareholders. We believe this precedent has big ramifications for today, which we will address shortly.

For the last five decades the standard deviation (average volatility) of dividend growth (Column G) has been only 1.2%. Statistically, dividend growth by decade has been remarkably stable.

Dividend yield by decade is in the row just under dividend growth. The average dividend yield for the five decades is shown in column G as 3.5%. Total return is defined as price appreciation plus dividend yield. In our “Total Dividend Return,” we substitute dividend growth for price appreciation. Thus, “Total Dividend Return” is equal to dividend growth plus dividend yield.

Total Dividend Return by decade for the DJIA has ranged from a low of 7.5% for the first half of the current decade, to a high of 12.3% for the decade of the 1980s. The five-decade average for DJIA Total Dividend Return has been 9.2% (Column F), again with a miniscule standard deviation of 1.9%.

Our theory holds that in the long-run, the total return of a stock should be approximately equal to its dividend yield plus its dividend growth, or as we have explained here, its Total Dividend Return. The reason is simple. If a company is giving its shareholders their fair cut of the profits, it should show up in the stock price. The stock market is a pricing machine. The more transparent a company is with their dividend policy, the more accurately the market will price their stock.

The average Total Dividend Return of 9.2% over the last five decades should sound very familiar. If it does not, the bottom half of Table 3 will refresh your memory. For the last five decades, the Dow Jones Industrial Average has averaged an annual total return of 10%, as shown in Column F. This has consisted of 6.5% average price growth and 3.5% average dividend yield (Column F).

It is eye opening that Total Dividend Return and total return in the DJIA have been so similar. Investors could have ignored the news of recessions, wars, oil shocks, assassinations, and tech bubbles. They could have dropped their subscriptions to the Wall Street Journal and pulled the plug on the talking heads on CNBC. They could have breathed easier each time a crisis of any kind came along; indeed, they could have dramatically reduced the time they invested in keeping up with the Dow Joneses. Instead, they could have watched just two things, the dividend growth and the dividend yield of the DJIA, and achieved over 90% of the rate of return of the index. But of equal importance, they could have done so with 75% less volatility than with the DJIA itself. The standard deviation of the Total Dividend Return as shown in Column F has been only 1.9% on an average return of 9.2%. This is in sharp contrast to the 7.4% standard deviation of the DJIA on its 10% average annual return.

We believe viewing the stock market or an individual stock from a dividend perspective is the right approach for most people. Dividends not only contribute directly to investment returns because they are real money, but they also have predictive powers for stock price appreciation, as well.

Table II has a lot going on, so let us describe the major points we will be discussing. The table shows the rates of returns for prices and dividends and the variability of the returns over the last five decades of the Dow Jones Industrial Average. The table compares the well-known concept of investment total return with our less well known “Total Dividend Return.” Our purpose in showing this table is to complete our discussion of a point we brought up earlier about dividends. We said the following:

“Importantly, our research shows that in the case of the DJIA, the steadily rising dividends have not only increased the investment returns they have also provided an important indication of the valuation of the DJIA itself. . . .”

At Donaldson Capital Management, we often say that many of our companies’ dividends are consistent and persistent. Just how consistent they are may surprise you. Earlier we said that the cumulative dividends of the DJIA have risen about 8 out every 10 years. The upper half of Table II shows dividend growth and dividend yield over the last five decades. Column A shows in the 1960s dividends grew by an average of 5.8% per year. Column F reveals that the average dividend growth for the last five decades has been 5.7%. The chart vividly shows that dividend growth has been very consistent during this time, with only the 7.6% growth in 1980s diverging very far from the growth of the other decades. We investigated this divergence and found that it was driven by the large dividend increases that companies made in 1987 and 1988. This was in the aftermath of the stock market crash in 1987, and we believe the outsized increases were the DJIA companies’ attempt to reassure their shareholders. We believe this precedent has big ramifications for today, which we will address shortly.

For the last five decades the standard deviation (average volatility) of dividend growth (Column G) has been only 1.2%. Statistically, dividend growth by decade has been remarkably stable.

Dividend yield by decade is in the row just under dividend growth. The average dividend yield for the five decades is shown in column G as 3.5%. Total return is defined as price appreciation plus dividend yield. In our “Total Dividend Return,” we substitute dividend growth for price appreciation. Thus, “Total Dividend Return” is equal to dividend growth plus dividend yield.

Total Dividend Return by decade for the DJIA has ranged from a low of 7.5% for the first half of the current decade, to a high of 12.3% for the decade of the 1980s. The five-decade average for DJIA Total Dividend Return has been 9.2% (Column F), again with a miniscule standard deviation of 1.9%.

Our theory holds that in the long-run, the total return of a stock should be approximately equal to its dividend yield plus its dividend growth, or as we have explained here, its Total Dividend Return. The reason is simple. If a company is giving its shareholders their fair cut of the profits, it should show up in the stock price. The stock market is a pricing machine. The more transparent a company is with their dividend policy, the more accurately the market will price their stock.

The average Total Dividend Return of 9.2% over the last five decades should sound very familiar. If it does not, the bottom half of Table 3 will refresh your memory. For the last five decades, the Dow Jones Industrial Average has averaged an annual total return of 10%, as shown in Column F. This has consisted of 6.5% average price growth and 3.5% average dividend yield (Column F).

It is eye opening that Total Dividend Return and total return in the DJIA have been so similar. Investors could have ignored the news of recessions, wars, oil shocks, assassinations, and tech bubbles. They could have dropped their subscriptions to the Wall Street Journal and pulled the plug on the talking heads on CNBC. They could have breathed easier each time a crisis of any kind came along; indeed, they could have dramatically reduced the time they invested in keeping up with the Dow Joneses. Instead, they could have watched just two things, the dividend growth and the dividend yield of the DJIA, and achieved over 90% of the rate of return of the index. But of equal importance, they could have done so with 75% less volatility than with the DJIA itself. The standard deviation of the Total Dividend Return as shown in Column F has been only 1.9% on an average return of 9.2%. This is in sharp contrast to the 7.4% standard deviation of the DJIA on its 10% average annual return.

We believe viewing the stock market or an individual stock from a dividend perspective is the right approach for most people. Dividends not only contribute directly to investment returns because they are real money, but they also have predictive powers for stock price appreciation, as well.

Tuesday, March 07, 2006

Donaldson Capital's General Dividend Strategy: Part I

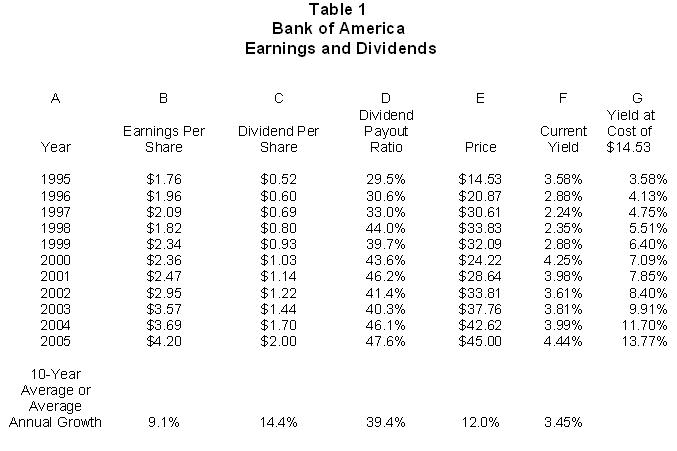

For example, Bank of America (BAC) pays a dividend of $2.00 and is selling at $45.00 per share, producing a current dividend yield of 4.44%. Although a yield of 4.44% is attractive, particularly in a world where a 10-year US Treasury Bond yields just over 4.0%, our research shows conclusively that it is the combination of dividend yield and dividend growth that offers the greatest rewards. BAC is one of our favorite stocks, but we like it for important reasons beyond its current dividend yield. Indeed, if its current dividend yield were all we could expect over the next 10 years, we would buy the Treasury bond because it is backed by the full faith and credit of the US government, while BAC's dividend is not guaranteed and could be cut to zero next week without violating any laws.

Quality Door

It is important to remember that dividends are not a legal obligation; they are paid at the sole discretion of the board of directors of the company. That is why, even though we invest only in stocks that pay dividends, our investment selection process does not start by going through the "Dividend Door." That process starts through the "Quality Door." By this we mean that all of our potential portfolio holdings must possess solid creditworthiness before we will even look at them from a dividend perspective. Indeed, the first question we ask about companies we are considering is -- would we loan them money? We expect to own most of the companies we buy for many years. Over time, some sort of bad news inevitably hits all companies. We want to be sure that the companies we own can take these hits and continue on without coming apart. The idea that you can jump in and out of stocks and avoid the hits is widespread among investors today and is simply not true. We can cite countless examples of where bad news has hit a company without warning, severely testing the financial and management resources of the organization for years, and never giving traders a prayer of getting their money back.

Most high-yield dividend stocks we see touted in the media can not pass through the quality door test. We think they are an accident waiting to happen. The companies are using high dividends just to keep investors happy, but they are, essentially, liquidating their companies by paying out more than they can afford. When the inevitable bad news comes, their high dividend will be the first thing to go.

If we were to reduce our investment selection process to one sentence it would be:

We seek to own companies with unquestioned financial strength that pay a generous dividend and promise superior dividend growth in the future.

The word dividend comes from the French word, dividere, meaning, to cut. Dividends are literally your "cut" of the company's profits, and herein lies the first hidden value of rising dividend investing: In selected companies, dividends go up almost every year. Indeed, in the last 45 years, the cumulative dividends of the Dow Jones Industrial Average (DJIA) have risen 37 times and fallen only 8 times. Few people are aware just how stable the dividends of some major companies really are. Another hidden value is that for the DJIA, the steadily rising dividends have not only represented nearly 40% of the DJIA's total investment return, they have also provided an important gauge for determining the value of the DJIA itself. We will elaborate on this idea later.

Yield at Cost

The current dividend yield of a stock whose dividend is stable is easily understood. You do not even need to know the formula because it is computed for you and shown in most financial publications for every stock. When you look at BAC in the paper or at an online financial site, it will look something like this:

For example, Bank of America (BAC) pays a dividend of $2.00 and is selling at $45.00 per share, producing a current dividend yield of 4.44%. Although a yield of 4.44% is attractive, particularly in a world where a 10-year US Treasury Bond yields just over 4.0%, our research shows conclusively that it is the combination of dividend yield and dividend growth that offers the greatest rewards. BAC is one of our favorite stocks, but we like it for important reasons beyond its current dividend yield. Indeed, if its current dividend yield were all we could expect over the next 10 years, we would buy the Treasury bond because it is backed by the full faith and credit of the US government, while BAC's dividend is not guaranteed and could be cut to zero next week without violating any laws.

Quality Door

It is important to remember that dividends are not a legal obligation; they are paid at the sole discretion of the board of directors of the company. That is why, even though we invest only in stocks that pay dividends, our investment selection process does not start by going through the "Dividend Door." That process starts through the "Quality Door." By this we mean that all of our potential portfolio holdings must possess solid creditworthiness before we will even look at them from a dividend perspective. Indeed, the first question we ask about companies we are considering is -- would we loan them money? We expect to own most of the companies we buy for many years. Over time, some sort of bad news inevitably hits all companies. We want to be sure that the companies we own can take these hits and continue on without coming apart. The idea that you can jump in and out of stocks and avoid the hits is widespread among investors today and is simply not true. We can cite countless examples of where bad news has hit a company without warning, severely testing the financial and management resources of the organization for years, and never giving traders a prayer of getting their money back.

Most high-yield dividend stocks we see touted in the media can not pass through the quality door test. We think they are an accident waiting to happen. The companies are using high dividends just to keep investors happy, but they are, essentially, liquidating their companies by paying out more than they can afford. When the inevitable bad news comes, their high dividend will be the first thing to go.

If we were to reduce our investment selection process to one sentence it would be:

We seek to own companies with unquestioned financial strength that pay a generous dividend and promise superior dividend growth in the future.

The word dividend comes from the French word, dividere, meaning, to cut. Dividends are literally your "cut" of the company's profits, and herein lies the first hidden value of rising dividend investing: In selected companies, dividends go up almost every year. Indeed, in the last 45 years, the cumulative dividends of the Dow Jones Industrial Average (DJIA) have risen 37 times and fallen only 8 times. Few people are aware just how stable the dividends of some major companies really are. Another hidden value is that for the DJIA, the steadily rising dividends have not only represented nearly 40% of the DJIA's total investment return, they have also provided an important gauge for determining the value of the DJIA itself. We will elaborate on this idea later.

Yield at Cost

The current dividend yield of a stock whose dividend is stable is easily understood. You do not even need to know the formula because it is computed for you and shown in most financial publications for every stock. When you look at BAC in the paper or at an online financial site, it will look something like this:

Name>>>Price>>> High>>> Low>>> Volume>>> PE>>> Dividend Yield BAC >>>>45 >>>>46.25>>> 44.15>>> 300,000 >12>>>> 2.00>>> 4.4

But, understanding the value of a rising dividend is much tougher and techniques to assist you in doing so are almost totally absent in today's media. One approach we use to uncover this hidden value is the concept of "Yield at Cost." Yield at Cost is the current dividend divided by your original purchase price. Yield at Cost is quite revealing once you understand how to use it. Let us show a Yield at Cost analysis for BAC. Most investors look only at price. Some might look at PE or yield, but almost no one will look at the most important data on the line, dividend. Let's say you bought BAC ten years ago. Table 1 on the next page shows that in 1995 you would have paid $14.53 per share for BAC. Dividing the current dividend of $2.00 by your original purchase price, we find that your Yield at Cost is 13.77%. This is a remarkable cash on cash return, yet no financial publication in the world can show it to you, because it is yours and yours alone. Looking at Table 1, you will see that in 1995 BAC paid a dividend of $.52, which produced a dividend yield of 3.58%. Over the last 10 years, however, the company has raised its dividend every year and today pays $2.00, almost four times what it paid in 1995. Please note that BAC's current yield, as would have been reported in the media, ranged between 2.25% and 4.44% (Column F). Your Yield at Cost, which Column G shows was rising every year, would have been completely hidden from you, unless you understood the concept. Let's look at Table 1 to see other important features of dividend investing.

Please double click the table to enlarge it.

If you are like most people, who look only at price, you wake up every morning saying, "Should I sell my BAC and take my profit, or should I wait for another day when it might be higher?" Our guess is that most price-only investors who bought BAC in 1995 had a very tough time holding the stock in the late 1990s. The stock went flat from 1997 through 2002 (Column E), at a time when the investment world became inebriated with tech stocks. Yet, even though BAC's price was going nowhere, its dividend and underlying value were increasing by double digits every year. BAC's dividend went from $.69 in 1997 to a $1.22 in 2002. That is nearly an 80% increase in cash distributions and the price hardly moved. That alone should have been a warning that something was amiss with the market's valuation mechanism. In hindsight, it is now clear that during this time something other than valuation was driving stock prices. That something was the irrational exhuberance for the thin air of high flying techs. Understanding that your Yield at Cost was rising every year, may have given you enough incentive not to go chasing tech stocks that were trading at 200 and 300 times earnings.

As shown in columns B and C, BAC's earnings and dividends have had average annual growth of 9.1% and 14.4%, respectively. This is excellent growth, particularly in dividends. Column D shows that BAC's dividend payout has averaged 39.4% of earnings per share. Column D also shows that the dividend payout ratio has been rising significantly with dividends representing about 30% of earnings ten years ago and about 50% today. This is graphic evidence of a board of directors that is able and willing to return to its shareholders a fair cut of the profits. Column E shows that BAC has experienced price growth of 12% per year, which is similar to dividend growth, as is often the case with rising dividend stocks. To determine BAC's average annual total return, we add the average annual dividend yield of 3.45% to the average annual price increase of 12% to arrive at 15.45%.

There is much good information on Table 1, but, as they say, the past results are no guarantee of the future, therefore, let me cite two points that suggest BAC's prospects for the next ten years are sound.

1. Growing Earnings: It is not well understood that the US economy has been growing on average about 7% a year for the last 50 years. If you are a closet economist you will fuss and say that the economy has grown at only 3% a year. But both numbers are correct. The more widely accepted figure of 3% annual growth is adjusted for inflation, which has averaged 4% per year during this time, and measures real economic growth. But the 7% figure is also correct because it is the actual or gross rate of economic growth not adjusted for inflation. Since stock prices and other corporate financial data are not adjusted for inflation, an apples to apples comparison calls for us to use the 7% growth rate.

BAC is as close to being a nationwide banking operation as any financial institution we have in this country. If the US economy continues to expand at a gross rate of 7% per year, it is not a stretch of the imagination to predict that BAC will also grow earnings at least at 7% annually for the next decade.

2. Precedents for a Continued Rising Dividend: So, BAC has a bright future. That does not mean its dividends will keep pace with its earnings. How can we be sure that the company's board of directors will continue to give us our cut? The short answer is we don't know. We believe the best way to judge a company's likelihood of being fair to its shareholders is to look for precedents from its past. In this case, we mean dividend decisions they made when things were tough. There is a powerful precedent-setting action contained in Table 1.

In 1998, BAC's earnings fell nearly 20% versus the prior year. Remarkably, BAC, showing their unquestioned financial strength, raised their dividend by nearly 14%. We see three good things to take from their actions:

A. They correctly saw that the troubles of the time were temporary.

B. They did not make a token dividend increase; they raised their dividend at the same rate as they had been doing prior to the earnings weakness.

C. Their strategic actions prior to 1998 created a strong financial condition that allowed them to handle the rough spot with ease. (Thus, the importance of the "Quality Door.")

If you are like most people, who look only at price, you wake up every morning saying, "Should I sell my BAC and take my profit, or should I wait for another day when it might be higher?" Our guess is that most price-only investors who bought BAC in 1995 had a very tough time holding the stock in the late 1990s. The stock went flat from 1997 through 2002 (Column E), at a time when the investment world became inebriated with tech stocks. Yet, even though BAC's price was going nowhere, its dividend and underlying value were increasing by double digits every year. BAC's dividend went from $.69 in 1997 to a $1.22 in 2002. That is nearly an 80% increase in cash distributions and the price hardly moved. That alone should have been a warning that something was amiss with the market's valuation mechanism. In hindsight, it is now clear that during this time something other than valuation was driving stock prices. That something was the irrational exhuberance for the thin air of high flying techs. Understanding that your Yield at Cost was rising every year, may have given you enough incentive not to go chasing tech stocks that were trading at 200 and 300 times earnings.

As shown in columns B and C, BAC's earnings and dividends have had average annual growth of 9.1% and 14.4%, respectively. This is excellent growth, particularly in dividends. Column D shows that BAC's dividend payout has averaged 39.4% of earnings per share. Column D also shows that the dividend payout ratio has been rising significantly with dividends representing about 30% of earnings ten years ago and about 50% today. This is graphic evidence of a board of directors that is able and willing to return to its shareholders a fair cut of the profits. Column E shows that BAC has experienced price growth of 12% per year, which is similar to dividend growth, as is often the case with rising dividend stocks. To determine BAC's average annual total return, we add the average annual dividend yield of 3.45% to the average annual price increase of 12% to arrive at 15.45%.

There is much good information on Table 1, but, as they say, the past results are no guarantee of the future, therefore, let me cite two points that suggest BAC's prospects for the next ten years are sound.

1. Growing Earnings: It is not well understood that the US economy has been growing on average about 7% a year for the last 50 years. If you are a closet economist you will fuss and say that the economy has grown at only 3% a year. But both numbers are correct. The more widely accepted figure of 3% annual growth is adjusted for inflation, which has averaged 4% per year during this time, and measures real economic growth. But the 7% figure is also correct because it is the actual or gross rate of economic growth not adjusted for inflation. Since stock prices and other corporate financial data are not adjusted for inflation, an apples to apples comparison calls for us to use the 7% growth rate.

BAC is as close to being a nationwide banking operation as any financial institution we have in this country. If the US economy continues to expand at a gross rate of 7% per year, it is not a stretch of the imagination to predict that BAC will also grow earnings at least at 7% annually for the next decade.

2. Precedents for a Continued Rising Dividend: So, BAC has a bright future. That does not mean its dividends will keep pace with its earnings. How can we be sure that the company's board of directors will continue to give us our cut? The short answer is we don't know. We believe the best way to judge a company's likelihood of being fair to its shareholders is to look for precedents from its past. In this case, we mean dividend decisions they made when things were tough. There is a powerful precedent-setting action contained in Table 1.

In 1998, BAC's earnings fell nearly 20% versus the prior year. Remarkably, BAC, showing their unquestioned financial strength, raised their dividend by nearly 14%. We see three good things to take from their actions:

A. They correctly saw that the troubles of the time were temporary.

B. They did not make a token dividend increase; they raised their dividend at the same rate as they had been doing prior to the earnings weakness.

C. Their strategic actions prior to 1998 created a strong financial condition that allowed them to handle the rough spot with ease. (Thus, the importance of the "Quality Door.")

Donaldson Capital Management has been using a dividend oriented investment approach since our founding. Dividend investing, a we practice it, is suited for those people who want their investments to be safe, to provide much higher than average cash flows, and over time to provide capital gains comparable to the blue chip averages with much less volatility.

Next time I will discuss the long-term statistical correlations between dividend growth and price growth. I think you will be surprised at the findings.

Blessings,

*All data shown here is taken from sources believed to reliable. DCM cannot guarantee their accuracy. Data may not total correctly due to rounding.

Wednesday, March 01, 2006

Wells Fargo on the Move

This move against the grain by WFC is a very good sign that high quality stocks are shaking off their lethargy. But WFC's move begs the question: why are they doing so well, when many banks have not done much pricewise in years? Furthermore, when a stock breaks to a new high in the face of headwinds, it usually means a change is near. What might that change be?

I think WFC's move is a signal that very high quality companies are on the march. I will show more examples later. It also makes the case that some very smart people are betting that the worries about the housing bubble may be overblown, because WFC is one of the country's largest mortgage originators. Finally, WFC's counterintuitive move may be based on the counterintuitive idea that slower overall economic growth would be good for the markets. That would mean that the 14 rate hikes by the Fed are finally starting to bite.

Whatever the reason, a company like WFC does not break to a new high because it gets touted on CNBC. It does so based on the valuation work by very large investors. Our model says WFC's most probable selling price by the end of 2006 will be at least $73.

This move against the grain by WFC is a very good sign that high quality stocks are shaking off their lethargy. But WFC's move begs the question: why are they doing so well, when many banks have not done much pricewise in years? Furthermore, when a stock breaks to a new high in the face of headwinds, it usually means a change is near. What might that change be?

I think WFC's move is a signal that very high quality companies are on the march. I will show more examples later. It also makes the case that some very smart people are betting that the worries about the housing bubble may be overblown, because WFC is one of the country's largest mortgage originators. Finally, WFC's counterintuitive move may be based on the counterintuitive idea that slower overall economic growth would be good for the markets. That would mean that the 14 rate hikes by the Fed are finally starting to bite.

Whatever the reason, a company like WFC does not break to a new high because it gets touted on CNBC. It does so based on the valuation work by very large investors. Our model says WFC's most probable selling price by the end of 2006 will be at least $73.