Saturday, December 24, 2005

Merry Christmas

A friend and client forwarded this email to me. It details many elements of the Christmas season and their meanings throughout history.

Merry Christmas to all, and to all goodnight,

http://www.deerlakemail.com/teach/

Monday, December 12, 2005

Valuation, Valuation, Valuation

I get people fussing with me all the time about the merits of dividend investing. These conversations go something like this: "The bottom line to me is the bottom line on my account statement," they say. "Dividends might be real money and be predictable, but they are not what makes a good investment. A good investment is one I buy low and sell high. Price growth and only price growth matters to me." If I hear this once a month, I hear it a dozen times a month. I hear it so often that it makes me think, I might have the privilege of working in this business for a long time because this kind of thinking is shortsighted, ill-informed, and costly.

Here's my bottom line. If you don't know what makes a stock go up, what good is the price rise to you. When do you take the profit--too soon, too late, never? The markets being what they are, the price will in time go down, and you won't understand that either. So you will cycle between "feeling" good when the market goes up and "feeling" bad when it goes down and have absolutely no idea which of your feelings is accurate. Moreover, as it relates to feelings and the stock markets, most likely neither of them is correct. Feelings are not facts in investing; not yours, not mine.

To escape the cycle of feelings and get connected to reality, you must develop some understanding of how to value a company. I have spent 20 years trying to do this, and my research shows that for many large companies the level and growth rate of their dividends is the best indicator of value. If you study the relationships between dividends and stock prices, you will be surprised by two things: 1. dividend trends are very consistent and persistent and much less volatile than prices or earnings; 2. and yet it is clear that prices follow dividends and not the other way around.

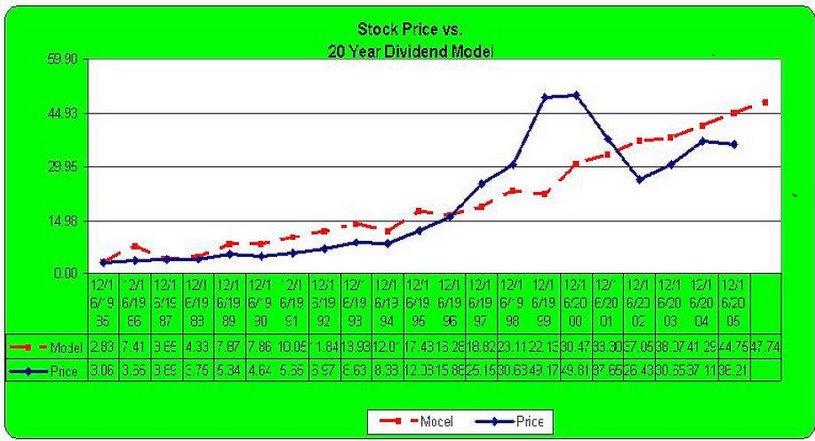

The Dividend Valuation chart below of General Electric is a good example of what I am talking about. The red line is our dividend valuation model for GE over the last 20 years. The Blue line is GE's actual price over this time. Many things are obvious with even a casual glance at the chart: first, the valuation line (red) is virtually a straight line, while the blue line showing price has been all over the road; second, the volatility of price has carried it back and forth across the valuation line; third, buying GE when its price was lower than its valuation line and selling it when its price was above the valuation line has been a near fool proof long-term strategy for the stock. Our rate of return is even better if we buy when price is 10% below valuation and sell when price is 10% above valuation. Finally, the chart shows that the model is signaling that GE is currently selling far below its valuation line, which would suggest it is a good buy. In fact the model is showing that GE is selling nearly 25% below its valuation line. Understanding the model as I do, the only way that the price of GE will now close the 25% gap is if its dividend growth slows dramatically or interest rates sky rocket, neither of which I believe is a strong possibility.

Investing always involves risk, but determining the value of a company keeps you from making emotional decisions that have little chance of success. But of even more importance is understanding value keeps you from getting shaken out of a cheap stock just because the price is going against you.

Someone is always trying to tell me I should be buying this stock or that one. When I ask why, the answer is almost always the same: "Because it's going up." Looking at the chart below, there were a lot of people who were touting GE in 1999, who are still underwater. But there is good news. By my calcuation, they will be back to break even in 2007.

-------GE Dividend Valuation Chart-------

Friday, December 02, 2005

UTX -- Of Horses and Hoods

I'm going to provide a look under the hood of one of our stock valuation models using United Technologies (UTX) as an example. Since 1988 the combination of UTX's dividend growth and the change in interest rates on a 10 Year US T-bond have explained 92% of the annual price movement of the stock. That model currently estimates that the current fair price range should be between $60 and $70 per share, with $65 being the midpoint of the range. UTX is now selling for $55 per share.

At today's price that puts UTX at as great a discount from expected value as at anytime in the last decade. But does that mean it is a table-pounding buy? Yes and no. The expected price range is well above UTX's current selling price, but a look at UTX's history shows that it has had periods of under and over valuation lasting up to 3 years. I fully expect UTX will reach $65 per share over the next few years, thus the question in my mind is not if, but when.

If UTX reaches $65 in the next year, it will produce a total return of approximately 18%; if it takes two years, we will make a little less than 9%. The reason I believe the odds favor UTX reaching $65 sooner rather than later is because UTX has already been undervalued for the past 12 months, so the averages are in our favor.

I just spoke to the company last week and tried to pry out of them what their dividend hike in 2006 might look like. They were noncommittal, except to say a dividend hike was likely in the first quarter. I told them they had enough free cash flow to choke a horse, and I thought their shareholders would applaud, another big dividend hike and a public statement about future hikes.

The company representative with whom I spoke was so used to talking with Wall Street analysts, who completely ignore dividends, that he seems a bit startled when I told him I would rather have the dividend hike than share buy backs.

I mentioned that I had read where the company was disappointed that its stellar 2005 results had largely been ignored by the market, I suggested that a commitment to a dividend payout ratio of 35% would do wonders for the stock price. He was a very pleasant man and said he would pass on my suggestion.

Let's put this one on our radar and see what the next dividend hike looks like. UTX is in our Rising Income Portfolio. Illinois Tool Works, which has a very similar story, is in our Blue Chip Growth Portfolio. I'll review it next.

Subscribe to:

Posts (Atom)